第1页共13页编号:时间:2021年x月x日书山有路勤为径,学海无涯苦作舟页码:第1页共13页CHAPTER16ANSWERSTOTEXTBOOKPROBLEMS1

Adeclineininvestmentdemanddecreasesthelevelofaggregatedemandforanyleveloftheexchangerate

Thus,adeclineininvestmentdemandcausestheDDcurvetoshifttotheleft

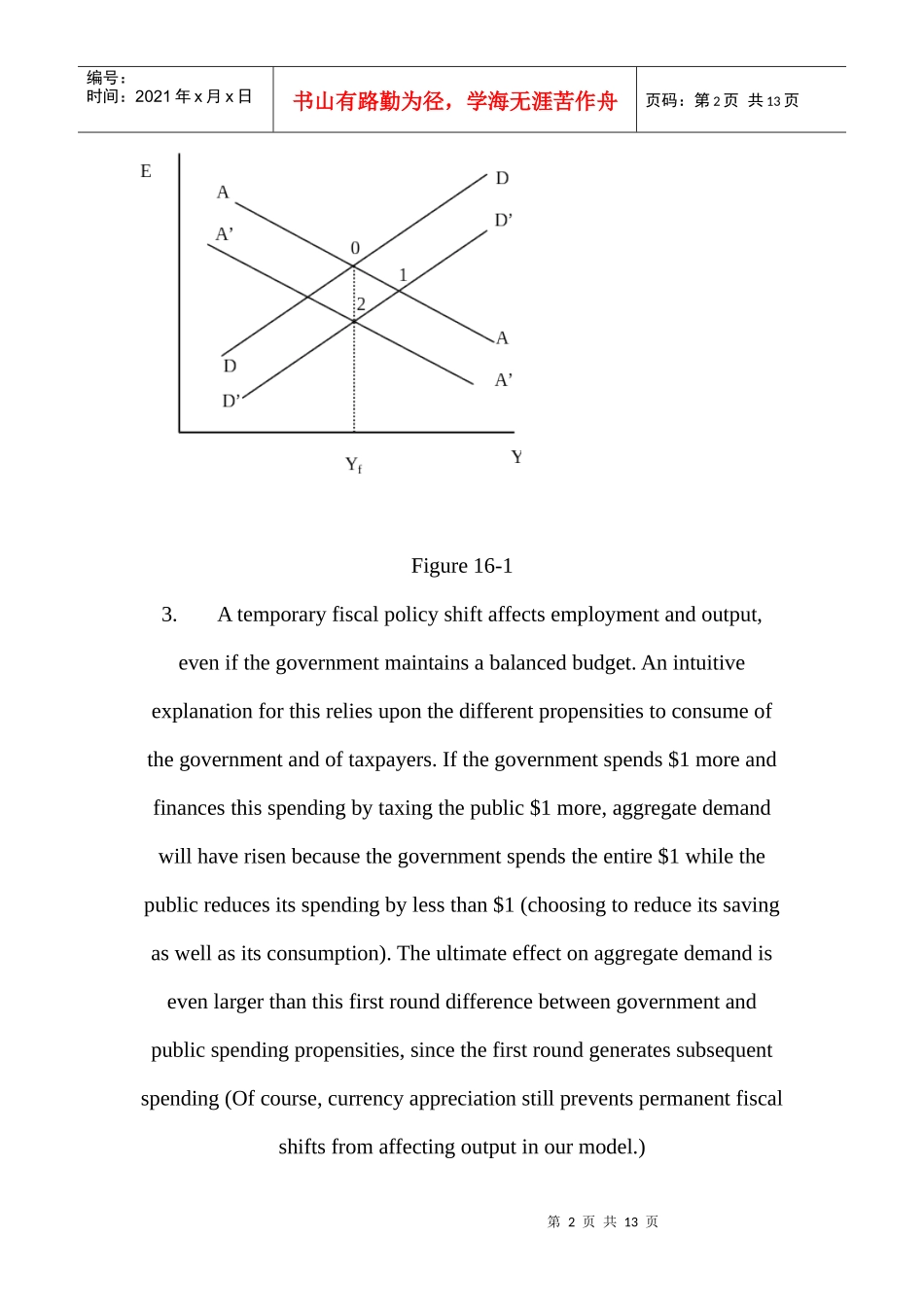

Atariffisataxontheconsumptionofimports

Thedemandfordomesticgoods,andthusthelevelofaggregatedemand,willbehigherforanyleveloftheexchangerate

Thisisdepictedinfigure16-1asarightwardshiftintheoutputmarketschedulefromDDtoD'D'

Ifthetariffistemporary,thisistheonlyeffectandoutputwillriseeventhoughtheexchangerateappreciatesastheeconomymovesfrompoint0topoint1

Ifthetariffispermanent,however,thelong-runexpectedexchangerateappreciates,sotheassetmarketscheduleshiftstoA'A'

Theappreciationofthecurrencyissharperinthiscase

Ifoutputisinitiallyatfullemploym