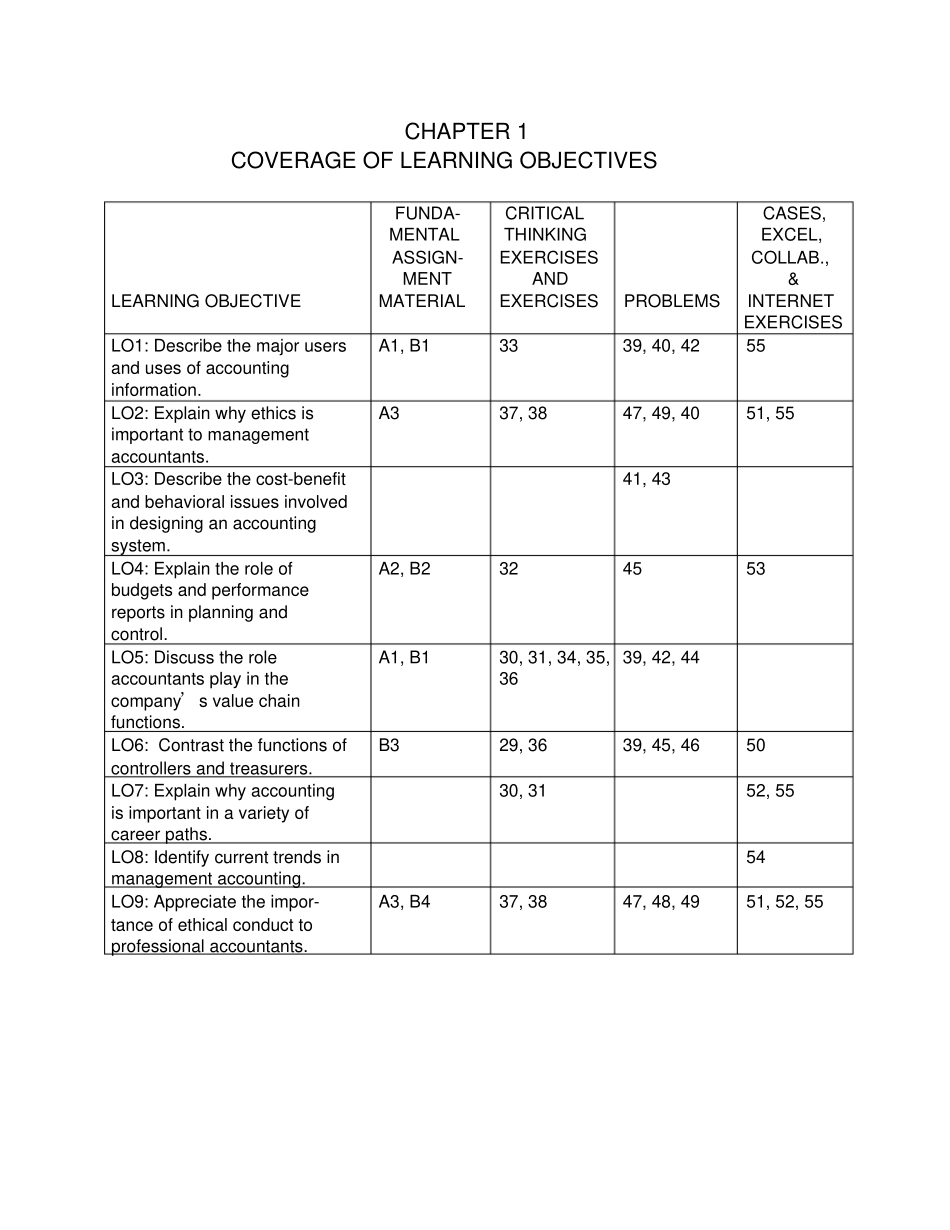

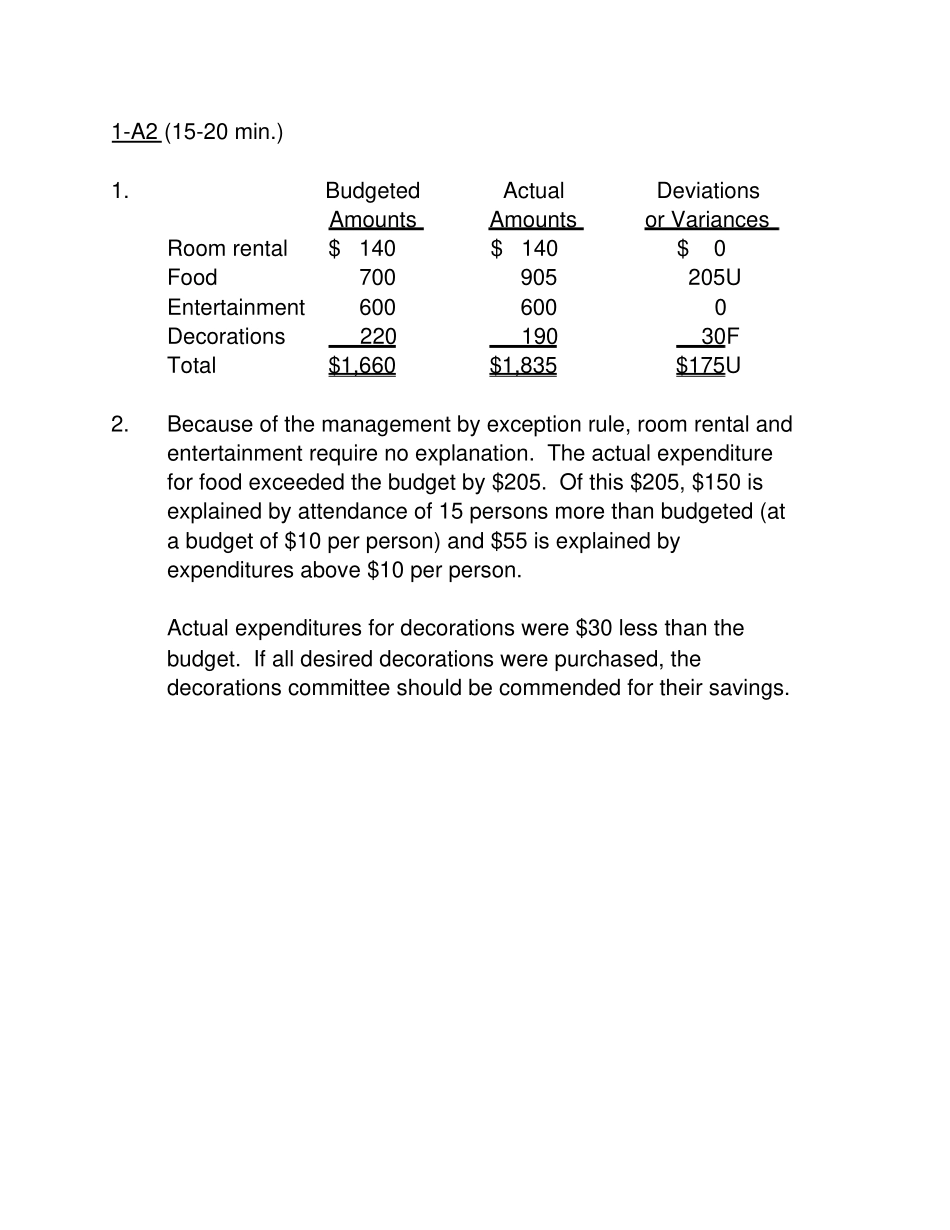

CHAPTER1COVERAGEOFLEARNINGOBJECTIVESLEARNINGOBJECTIVEFUNDA-MENTALASSIGN-MENTMATERIALCRITICALTHINKINGEXERCISESANDEXERCISESPROBLEMSCASES,EXCEL,COLLAB.,&INTERNETEXERCISESLO1:Describethemajorusersandusesofaccountinginformation.A1,B13339,40,4255LO2:Explainwhyethicsisimportanttomanagementaccountants.A337,3847,49,4051,55LO3:Describethecost-benefitandbehavioralissuesinvolvedindesigninganaccountingsystem.41,43LO4:Explaintheroleofbudgetsandperformancereportsinplanningandcontrol.A2,B2324553LO5:Discusstheroleaccountantsplayinthecompany’svaluechainfunctions.A1,B130,31,34,35,3639,42,44LO6:Contrastthefunctionsofcontrollersandtreasurers.B329,3639,45,4650LO7:Explainwhyaccountingisimportantinavarietyofcareerpaths.30,3152,55LO8:Identifycurrenttrendsinmanagementaccounting.54LO9:Appreciatetheimpor-tanceofethicalconducttoprofessionalaccountants.A3,B437,3847,48,4951,52,55CHAPTER1ManagerialAccounting,theBusinessOrganization,andProfessionalEthics1-A1(10-15min.)Becausetheaccountant'sdutiesoftenarenotsharplydefined,someoftheseanswerscouldbechallenged:1.Scorekeeping.Determiningadepreciationscheduleissimplyanexerciseinpreparingfinancialstatementstoreporttheresultsofactivities.2.Problemsolving.Helpsamanagerassesstheimpactofadecision.3.Scorekeeping.Reportsontheresultsofanoperation.Couldalsobeattentiondirectingifscrapisanareathatmightrequiremanagementdecisions.4.Attentiondirecting.Focusesattentiononareasthatneedattention.5.Attentiondirecting.Helpsmanagerslearnabouttheinformationcontainedinaperformancereport.6.Scorekeeping.Thestatementmerelyreportswhathashappened.7.Problemsolving.Thecostcomparisonisapparentlyusefulbecausethemanagerwishestodecidebetweentwoalternatives.Thus,itaidsproblemsolving.8.Attentiondirecting.Variancespointoutareaswhereresultsdifferfromexpectations.Interpretingthemdirectsattentiontopossiblecausesofthedifferences.9.Problemsolving.Aidsadecisionaboutwherethepartsshouldbemade.10.Attentiondirectingandproblemsolving.Budgetinginvolvesmakingdecisionsaboutplannedactivities--hence,aidingproblemsolving.Budgetsalsodirectattentiontoareasofopportunityorconcern--hence,directingattention.Reportingagainstthebudgetalsohasascorekeepingdimension.1-A2(15-20min.)1.BudgetedActualDeviationsAmountsAmountsorVariancesRoomrental$140$140$0Food700905205UEntertainment6006000Decorations22019030FTotal$1,660$1,835$175U2.Becauseofthemanagementbyexceptionrule,roomrentalandentertainmentrequirenoexplanation.Theactualexpenditureforfoodexceededthebudgetby$205.Ofthis$205,$150isexplainedbyattendanceof15personsmorethanbudgeted(atabudgetof$10perperson)and$55isexplainedbyexpendituresabove$10perperson.Actualexpendituresfordecorationswere$30lessthanthebudget.Ifalldesireddecorationswerepurchased,thedecorationscommitteeshouldbecommendedfortheirsavings.1-A3(10min.)Allofthesituationsraisepossibilitiesforviolationoftheintegritystandard.Inaddition,themanagerineachsituationmustaddressanadditionalethicalstandard:1.TheGeneralMillsmanagermustrespecttheconfidentialitystandard.Heorsheshouldnotdiscloseanyinformationaboutthenewcereal.2.Felixmustaddresshislevelofcompetencefortheassignment.Ifhissupervisorknowshislevelofexpertiseandwantsananalysisfroma“layperson”pointofview,heshoulddoit.However,ifthesupervisorexpectsanexpertanalysis,Felixmustadmithislackofcompetence.3.ThecredibilitystandardshouldcauseMarySuetodeclinetoomittheinformationfromh...