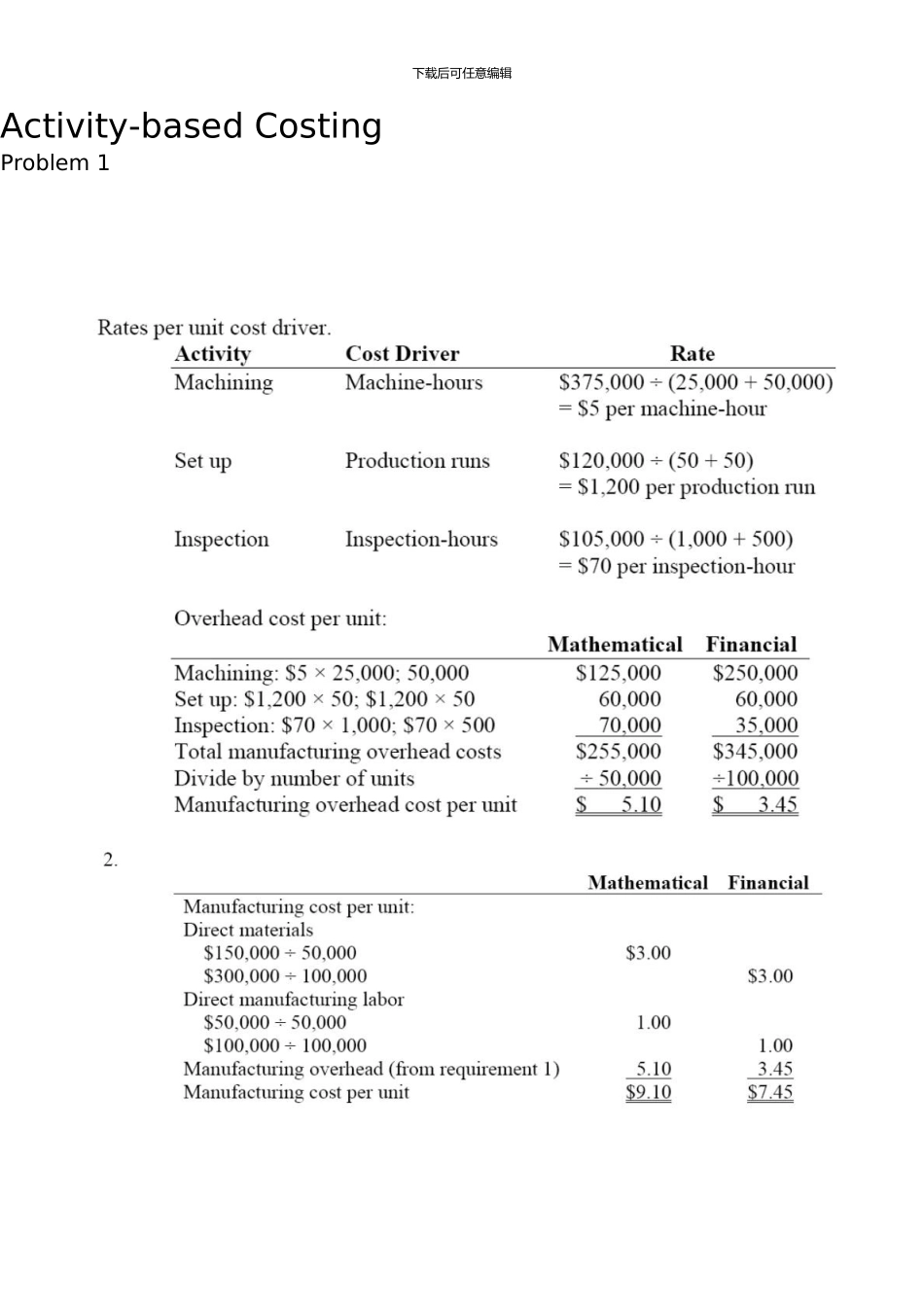

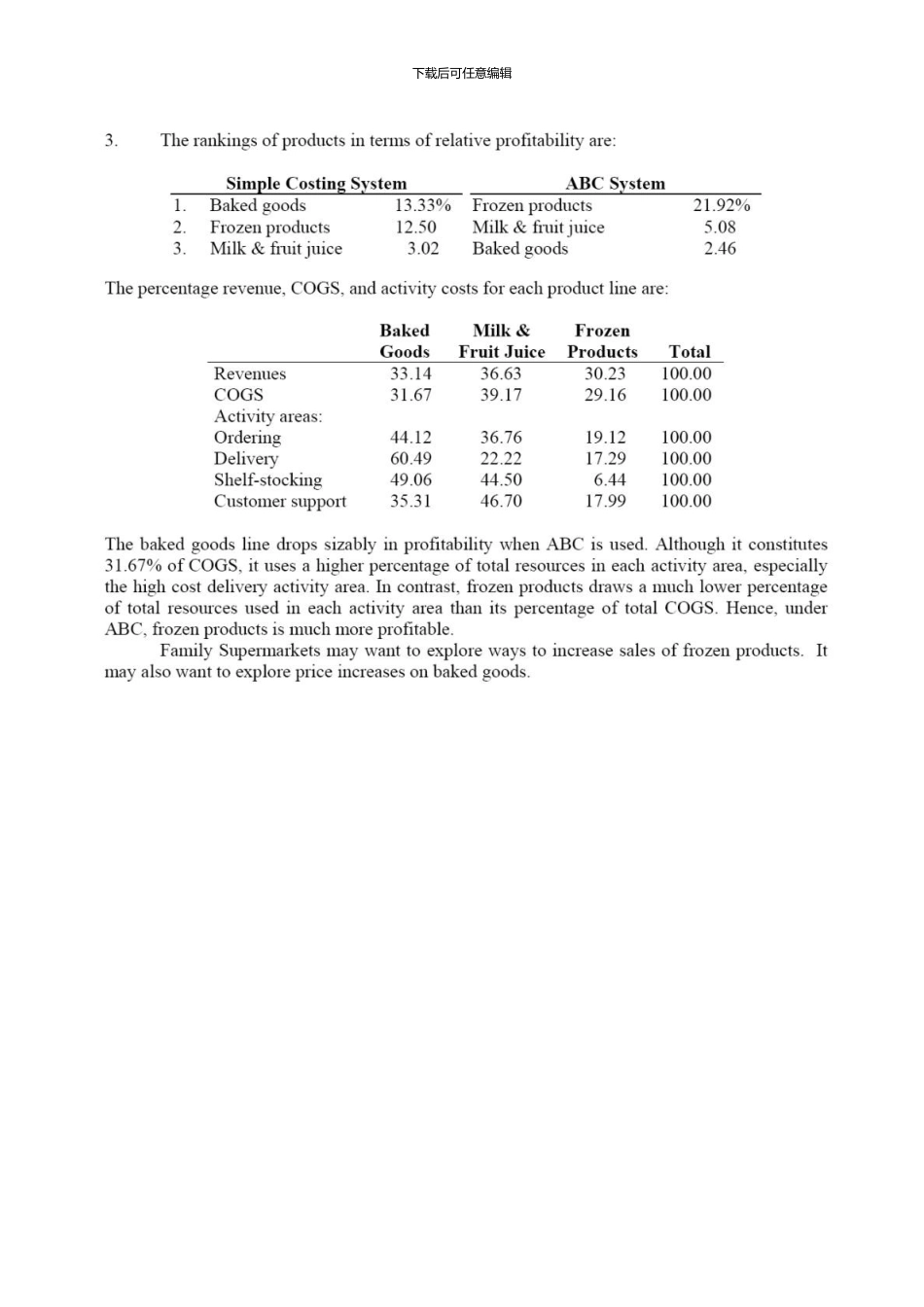

下载后可任意编辑 Activity‐based CostingProblem 1下载后可任意编辑 Problem 2下载后可任意编辑 下载后可任意编辑 Problem 31Total overhead:$520,000Costunitper$2

00Number of units260,000A2KTotal160,000 x 2

00100,000 x 2

00Total allocated$320,000$320,000200,000$520,000200,000$320,000A$200,000KTotal overheadNumber of unitsCost per unit$320,000160,000$2$200,000100,000$23ActivityAllocation$164,00040Cost per cost driver$4,100 per setupProduction setupsCostNumber of setupsMaterial handlingPackaging CostsCost$96,000160$600$1下载后可任意编辑per partNumber of partsCost$260,000260,000per partNumber of unitsProduction setups16 x $4100; 24 x $4100Material Handling112 x $600; 48 x $600PackagingAKTotal$65,600$98,400$164,00067,20028,80096,000160,000 x $1; 100,000 x $1Total cost allocated160,000100,000260,0004$292,800$227,200$520,000Total cost allocat