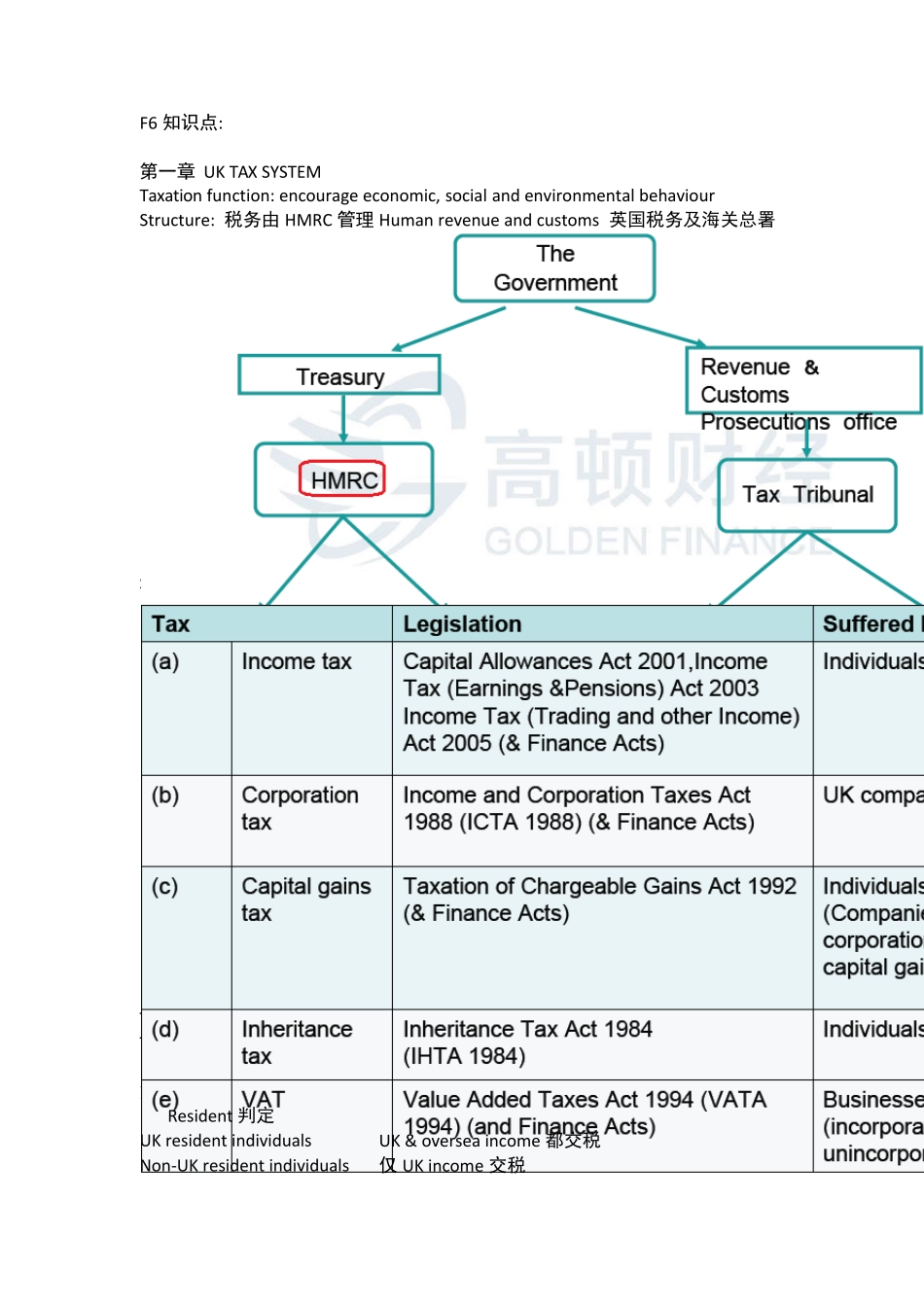

F6 知识点: 第一章 UK TAX SYSTEM Taxation function: encourage economic, social and environmental behaviour Structure: 税务由 HMRC 管理 Human revenue and customs 英国税务及海关总署 Source of law 立法 Finance Act 每年更新税率 Tax year: April 6th to April 5th Tax evasion is illegal 逃税非法 & Tax avoidance is legal 合理避税合法 第二章 Computation of taxable income and income tax liability 1

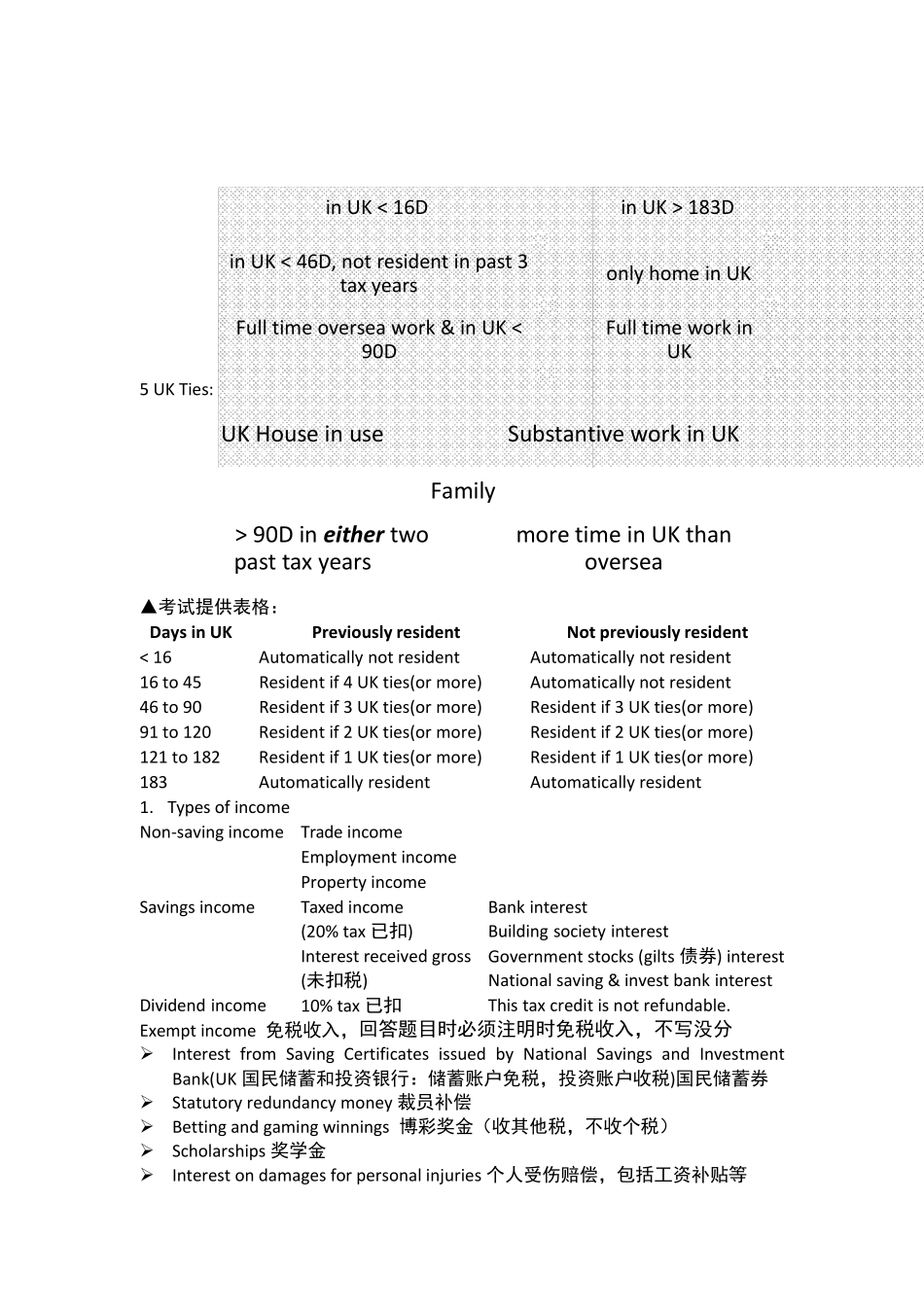

Resident 判定 UK resident individuals UK & oversea income 都交税 Non‐UK resident individuals 仅 UK income 交税 5 UK Ties: ▲考试提供表格: Days in UK Previously resident Not previously resident < 16 Automatically not resident Automatically not resident 16 to 45 Resident if 4 UK ties(or more) Automatically not resident 46 to 90 Resident if 3 UK ties(or more) Resident if 3 UK ties(or more) 91 to 120 Resident if 2 UK ties(or more) Resident if 2 UK ties(or more) 121