第五组金融资本市场字数:9304基于GARCH族的我国股指波动率的拟合及预测雷滔【摘要】近20年来使用GARCH类模型预测金融市场的波动率已成为该领域理论及实证上的热门话题

本文对我国沪深及香港恒生等主要股指收益的ARCH效应检验,使用GARCH类模型包括:GARCH(1,1)、GARCH-M及描述非对称的EGARCH和TGARCH模型来拟合股指的波动性,进行波动性的预测以及预测效果的评价是本文的四大核①心

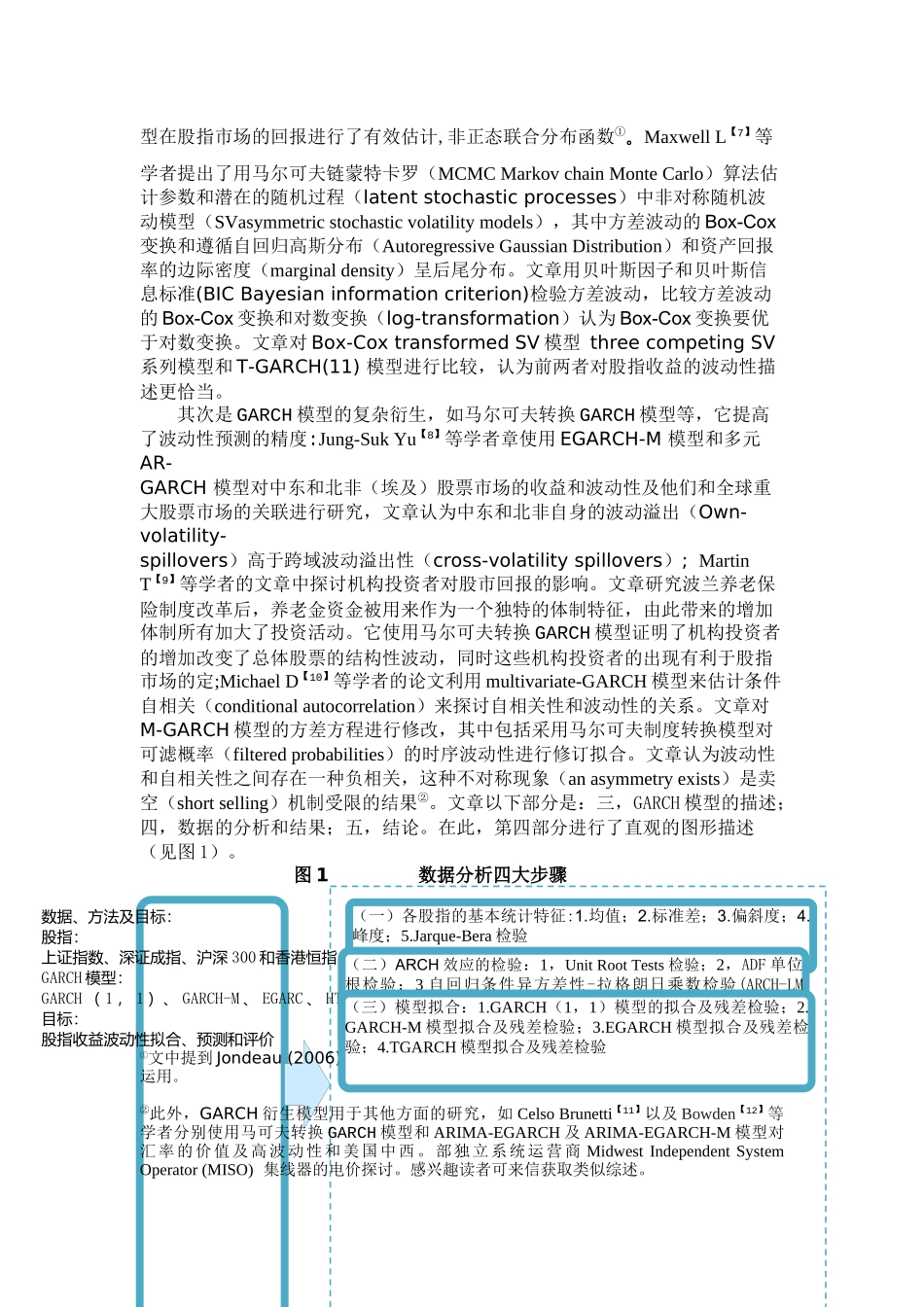

文章对最近两年GARCH模型的发展进行了全面综述,并对拟合预测评价进行了直观的图形描述

关键词:波动率;GARCH族;拟合;预测中图分类号F830文献标识码ATheGARCH-basedresearchonthefittingandpredictionofstockindex’svolatility【Abstract】Overthepast20years,theuseofGARCH-typemodelstopredictthefinancialmarketvolatilityhasbecomeahottopicbothintheoreticalandinempiricalarea

ThisarticlefocusonhavingtheARCHeffectstestontherevenueofstockindexrevenueinChina'sShanghai、ShenzhenandHongKong'sHangSengandothermajormarketusingofGARCH-typemodelsincluding:GARCH(11)、GARCH-MaswellasthedescriptionofasymmetricSuchasTGARCHandEGARCHmodelstofitthevolatilityofstockindexcarryingou