第1页共16页编号:时间:2021年x月x日书山有路勤为径,学海无涯苦作舟页码:第1页共16页时间序列分析第四次作业——房青B071209410712091531

ARMA-GARCHmodelingofSSECompositeIndex

Usetherecent1000obervationsonthelogreturnoftheSSECI

(1)UsePACFtoidentifyanARCHmodeloftheseries

Intermsofcorrelations,isthismodeladequateforthemodelingoftheconditionalheteroskedasicity

Andwhatabouttheconditionalmean

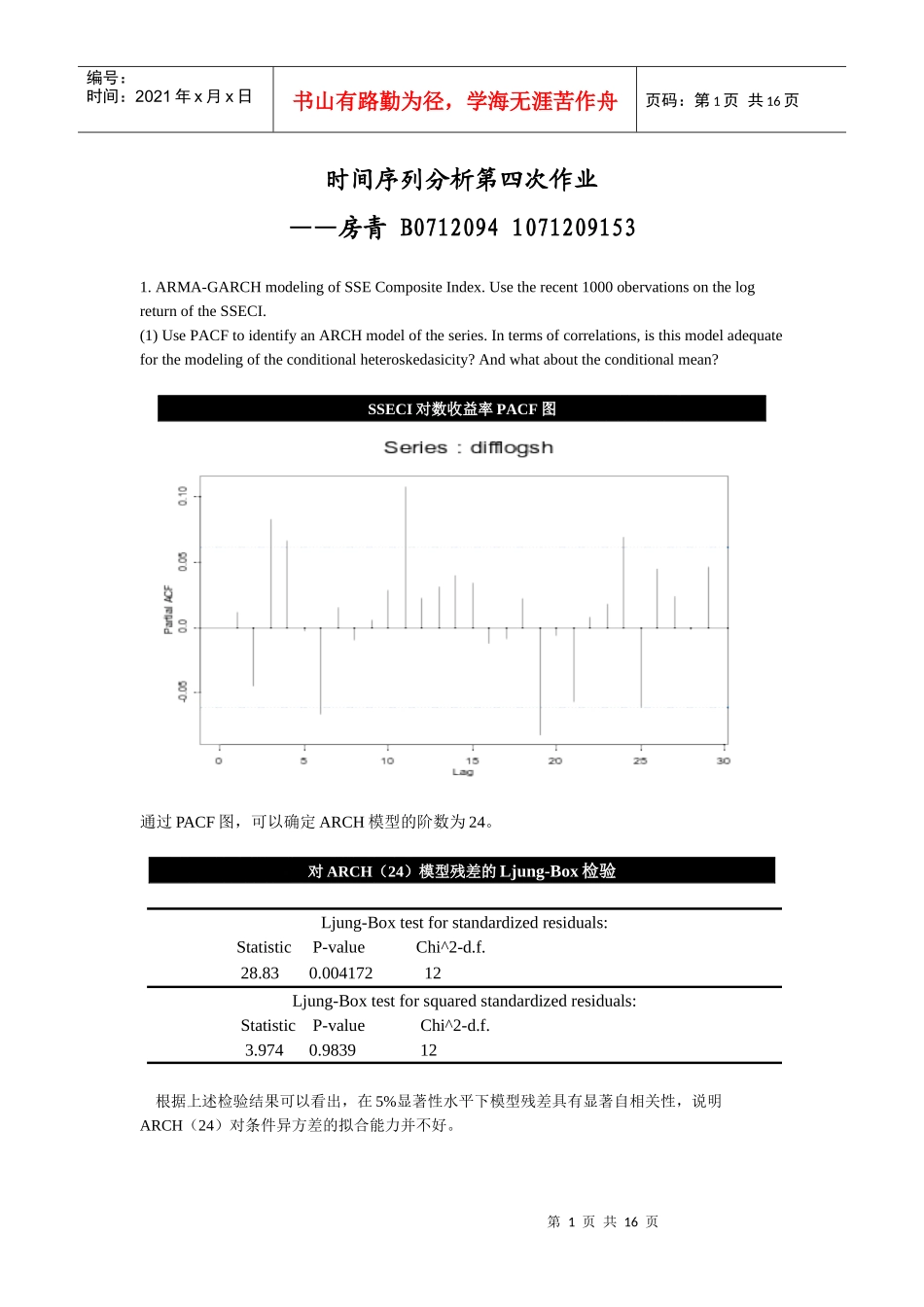

SSECI对数收益率PACF图通过PACF图,可以确定ARCH模型的阶数为24

对ARCH(24)模型残差的Ljung-Box检验Ljung-Boxtestforstandardizedresiduals:StatisticP-valueChi^2-d

00417212Ljung-Boxtestforsquaredstandardizedresiduals:StatisticP-valueChi^2-d

983912根据上述检验结果可以看出,在5%显著性水平下模型残差具有显著自相关性,说明ARCH(24)对条件异方差的拟合能力并不好

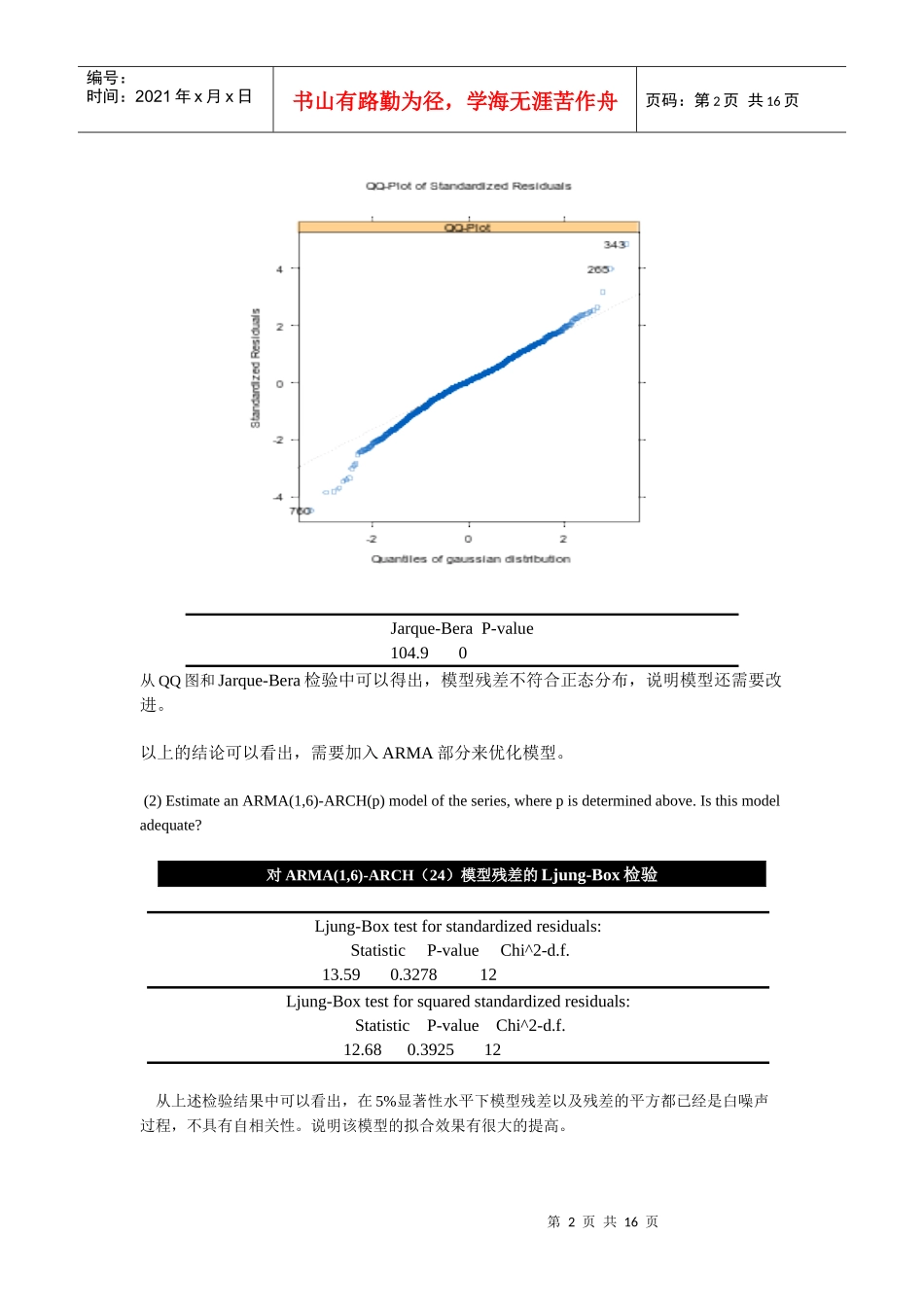

第2页共16页第1页共16页编号:时间:2021年x月x日书山有路勤为径,学海无涯苦作舟页码:第2页共16页Jarque-BeraP-value104

90从QQ图和Jarque-Bera检验中可以得出,模型残差不符合正态分布,说明模型还需要改进

以上的结论可以看出,需要加入ARMA部分来优化模型

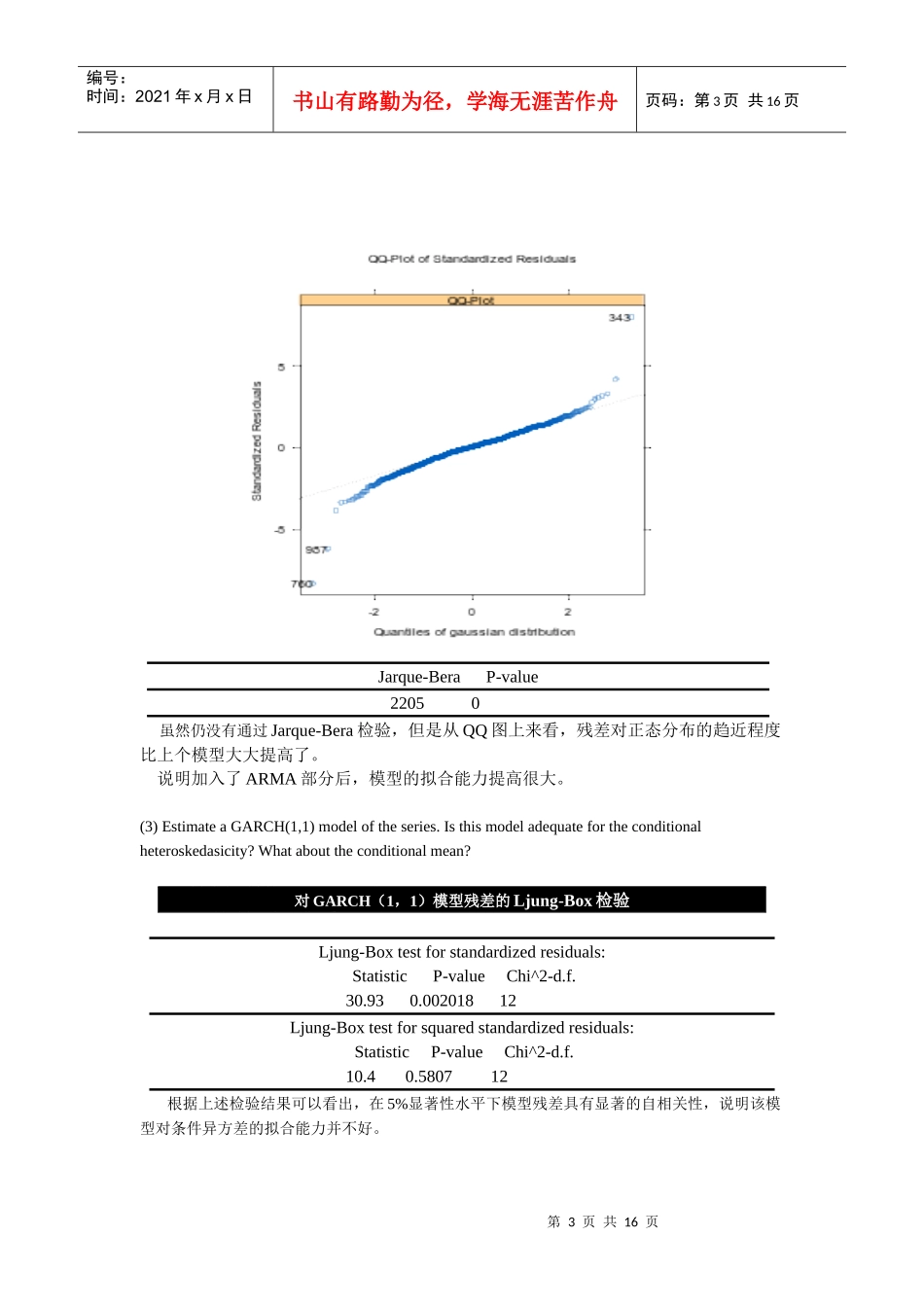

(2)EstimateanARMA(1,6)-ARCH