Copyright © 2011 Pearson Education, Inc

, Publishing as Prentice Hall

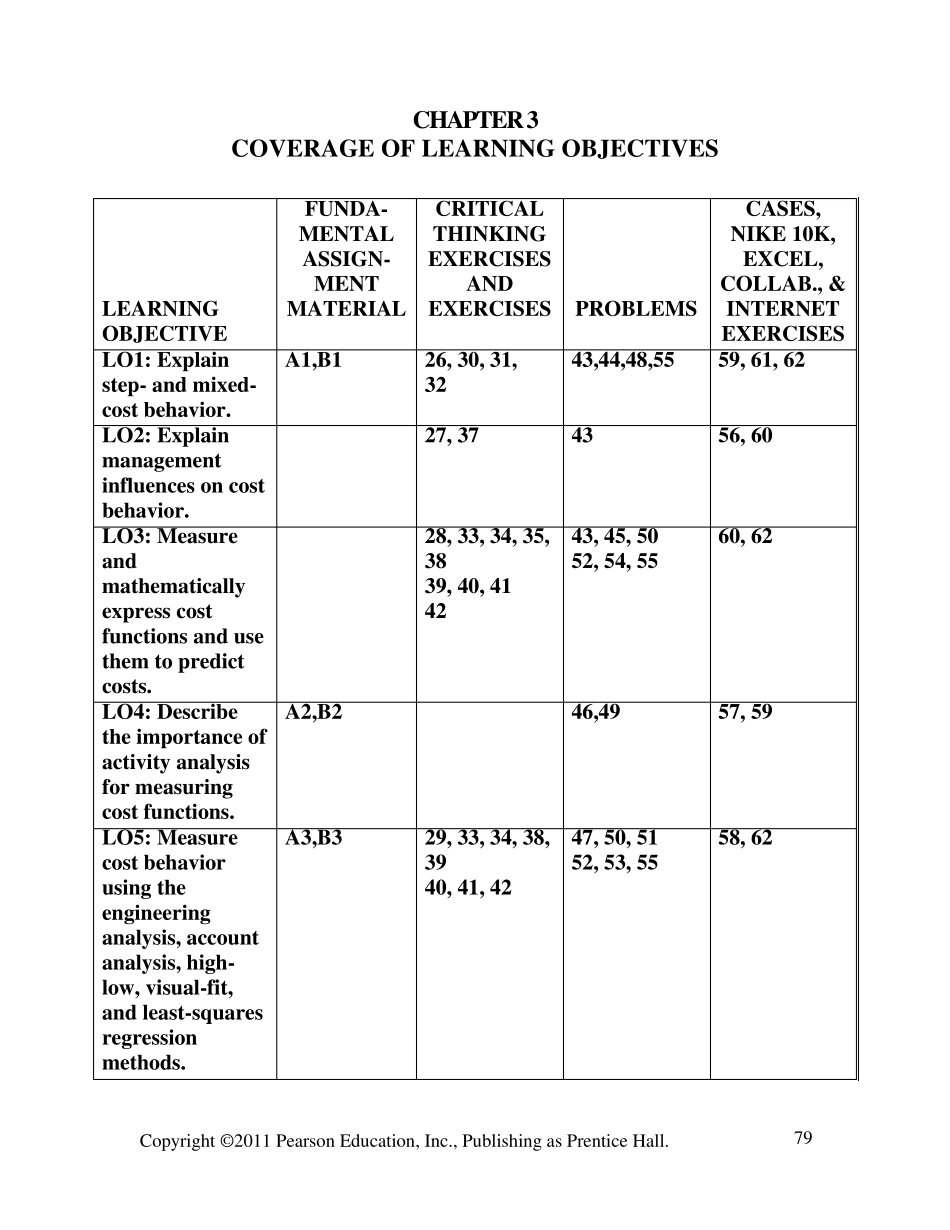

79 CHAPTER 3 COVERAGE OF LEARNING OBJECTIVES LEARNING OBJECTIVE FUNDA- MENTAL ASSIGN-MENT MATERIAL CRITICAL THINKING EXERCISES AND EXERCISES PROBLEMS CASES, NIKE 10K, EXCEL, COLLAB

, & INTERNET EXERCISES LO1: Explain step- and mixed-cost behavior

A1,B1 26, 30, 31, 32 43,44,48,55 59, 61, 62 LO2: Explain management influences on cost behavior

27, 37 43 56, 60 LO3: Measure and mathematically express cost functions and use them to predict costs

28, 33, 34, 35, 38 39, 40, 41 42 43, 45, 50 52, 54, 55 60, 62 LO4: Describe the importance of activity analysis for measuring cost functions

A2,B2 46,49 57, 59 LO5: Measure cost behavior using the engineering analysis, account analysis, high-low, visual-fit, and least-squares reg