35 第5 讲 ARIMA 模型预测案例 【例1】(1120070693)中国公路客运量ARIMA 模型(缺中间项的自回归模型) 中国公路客运量数据(19502005)序列与差分序列见图

0400,000800,0001,200,0001,600,0002,000,000505560657075808590950005Y-40,000040,00080,000120,000160,000200,000505560657075808590950005DY 序列存在异方差

应该用对数差分序列建立模型

789101112131415505560657075808590950005LNY-

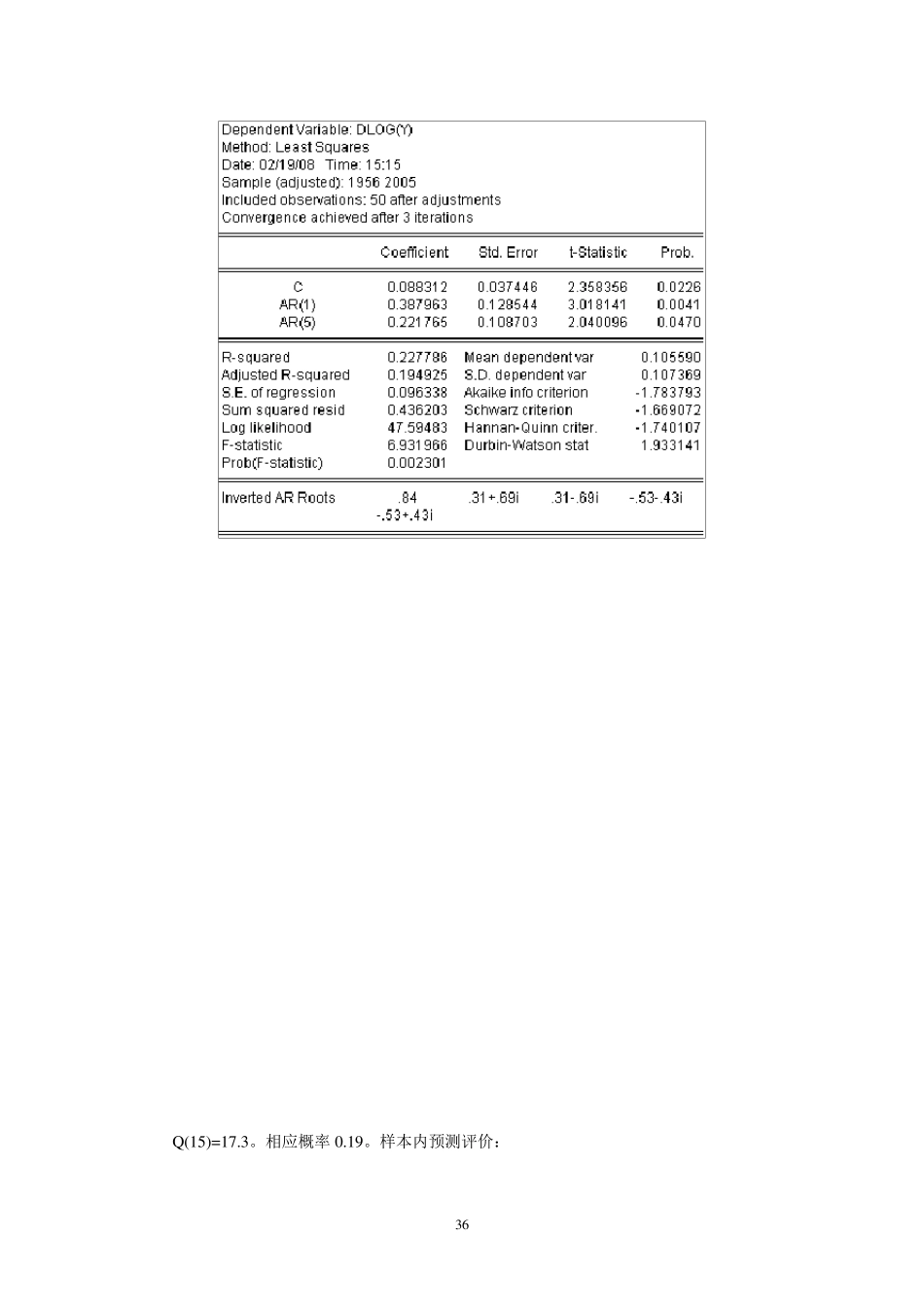

6505560657075808590950005DLNY Lny序列 DLny序列 建立 AR(5)模型 36 Q (15)=17

相应概率 0

样本内预测评价: 37 0400000800000120000016000002000000240000060657075808590950005YFForecast: YFActual: YForecast sample: 1950 2005Adjusted sample: 1956 2005Included observations: 50Root Mean Squared Error 34705

71Mean Absolute Error 19505

87Mean Abs

Percent Error 6

120935Theil Inequality Coefficient 0

023852 Bias Proportion 0

031884 Variance Proportion 0

104863 Covariance Proportion 0

863252 【例2】(1120070642)美元