GENERALIZEDRCAHMODELSWITHAPPLICATIONSFALL 2004R

Adam HoppesDepartment of StatisticsNorth Carolina State UniversityTABLE OF CONTENTSR

HOPPESContents1Introduction and Motivation11

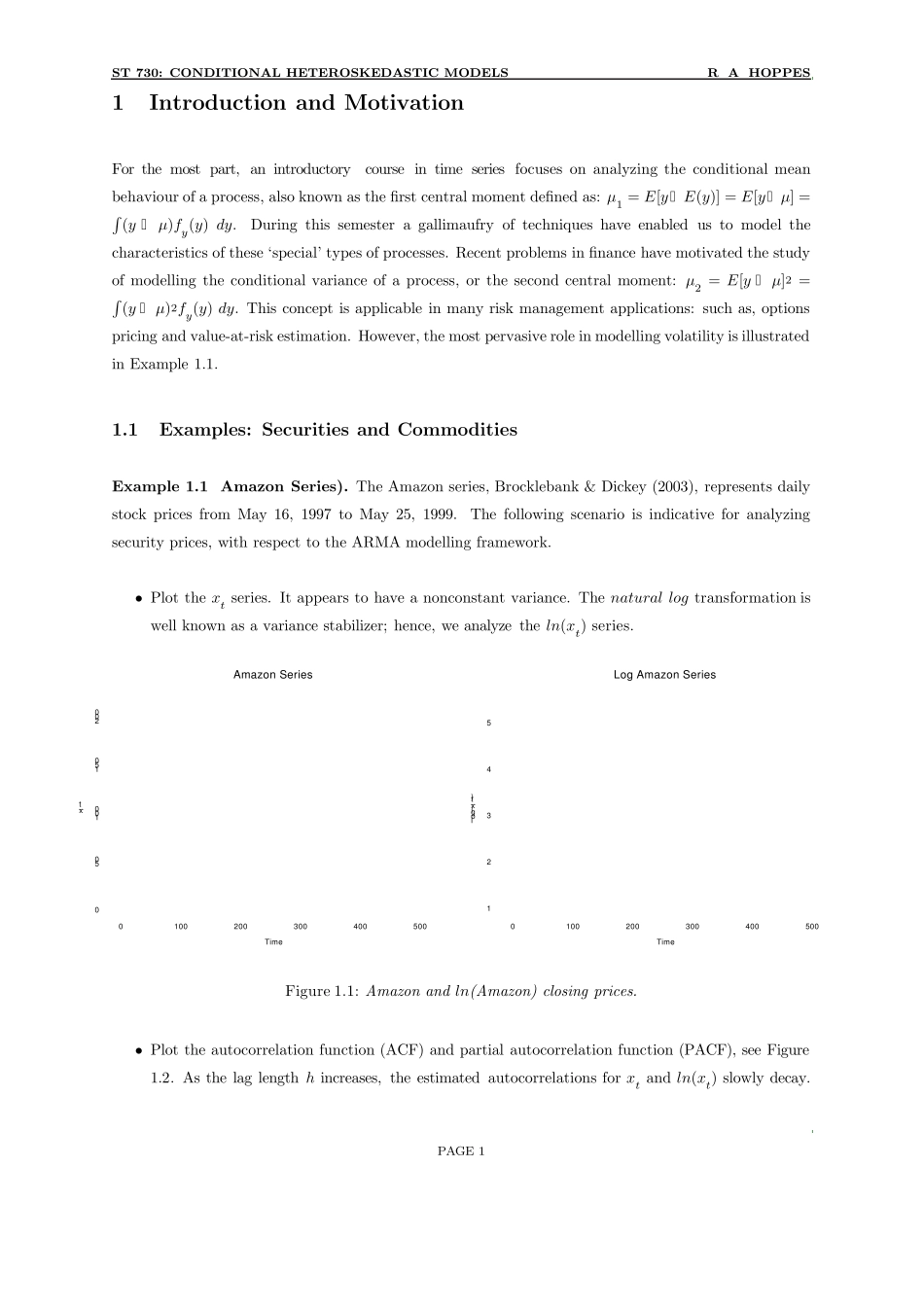

1Examples: Securities and Commodities

12Univariate ARCH Processes52

1ARCH(1) Model

2ARCH(p) Model

73Univariate GARCH Processes133

1GARCH(p, q) Model

2Extended GARCH(p, q) Models

144References15iST 730: CONDIT IONAL HET EROSKEDAST IC MODELSR

HOPPES