第458页共7页编号:时间:2021年x月x日书山有路勤为径,学海无涯苦作舟页码:第458页共7页《CorporateFinance》公司理财StephenA

Ross机械工业出版社Chapter31:InternationalCorporateFinance31

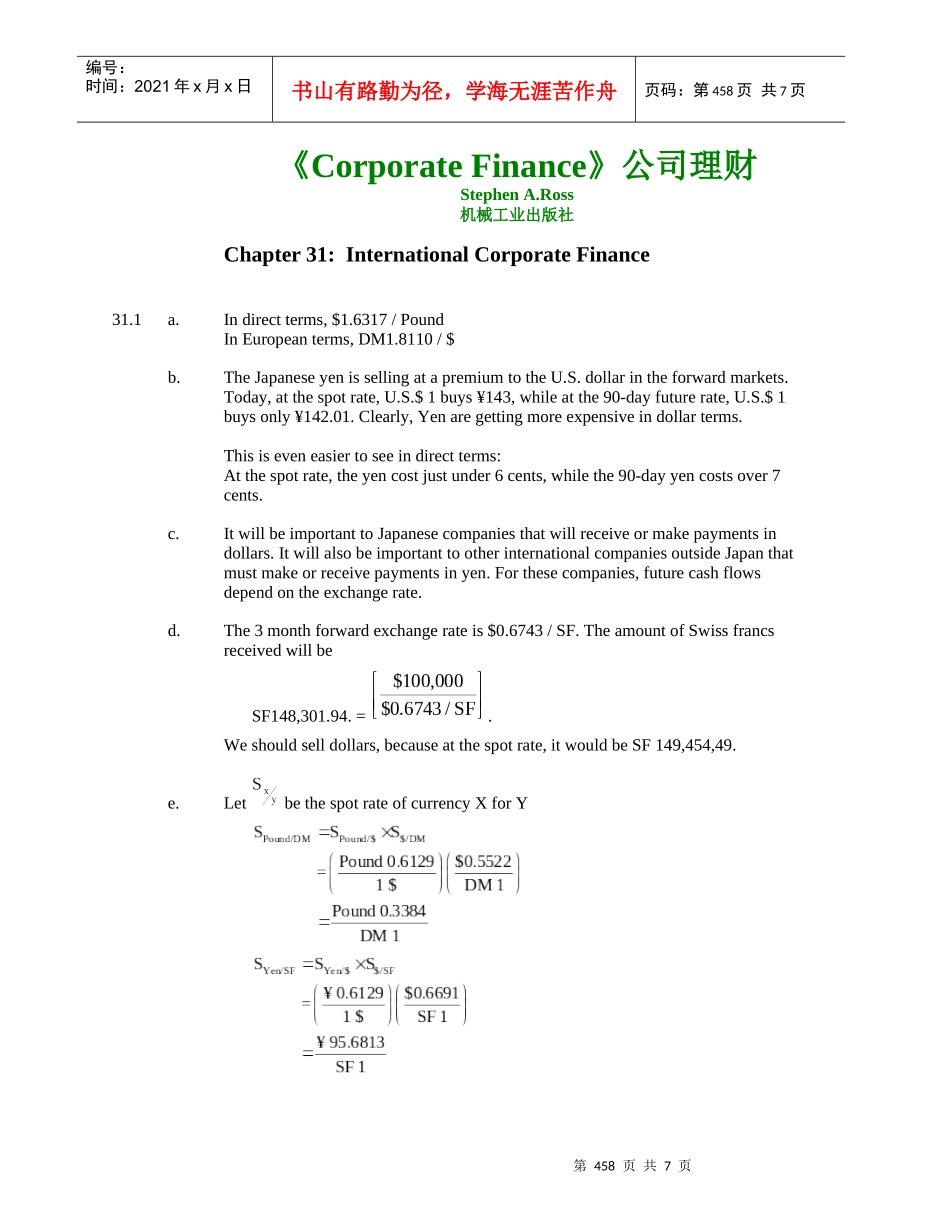

Indirectterms,$1

6317/PoundInEuropeanterms,DM1

8110/$b

TheJapaneseyenissellingatapremiumtotheU

dollarintheforwardmarkets

Today,atthespotrate,U

$1buys¥143,whileatthe90-dayfuturerate,U

$1buysonly¥142

Clearly,Yenaregettingmoreexpensiveindollarterms

Thisiseveneasiertoseeindirectterms:Atthespotrate,theyencostjustunder6cents,whilethe90-dayyencostsover7cents

ItwillbeimportanttoJapanesecompaniesthatwillreceiveormakepaymentsindollars

ItwillalsobeimportanttootherinternationalcompaniesoutsideJapanthatmustmakeorreceivepaymentsinyen

Forthesecompanies,futurecashflowsdependontheexchangerate

The3monthforwardexchangerateis$0

6743/SF

TheamountofSwissfrancsrecei