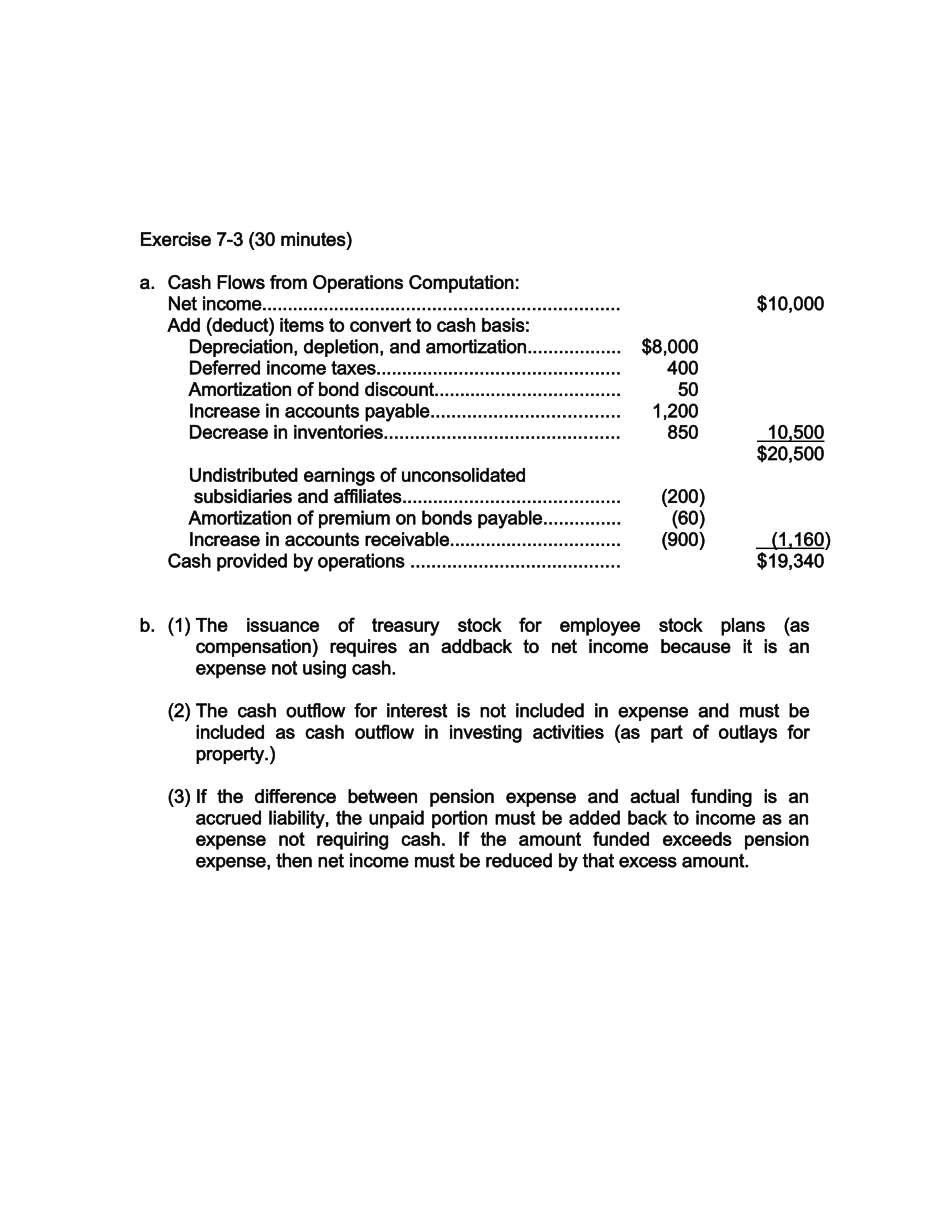

Exercise7-3(30minutes)a

CashFlowsfromOperationsComputation:Netincome

$10,000Add(deduct)itemstoconverttocashbasis:Depreciation,depletion,andamortization

$8,000Deferredincometaxes

400Amortizationofbonddiscount

50Increaseinaccountspayable

1,200Decreaseininventories

85010,500$20,500Undistributedearningsofunconsolidatedsubsidiariesandaffiliates

(200)Amortizationofpremiumonbondspayable

(60)Increaseinaccountsreceivable

(900)(1,160)Cashprovidedbyoperations