Samplequestion:Youhavethefollowingratesofreturnforariskyportfolioforseveralrecentyears:1

Ifyouinvested$1,000atthebeginningof2005yourinvestmentattheendof2008wouldbeworth___________

$2,176

$1,785

$1,645

$1,247

87Ifyouinvest1,000,attheendofyearone,youwillhave1000*(1+35

23%),Attheendofyear2,youwillhave1000*(1+35

23%)*(1+18

67%),dothesameworkforyear3and4,then$1000(1+35

23%)(1+18

67%)(1-9

87%)(1+23

45%)=$1785

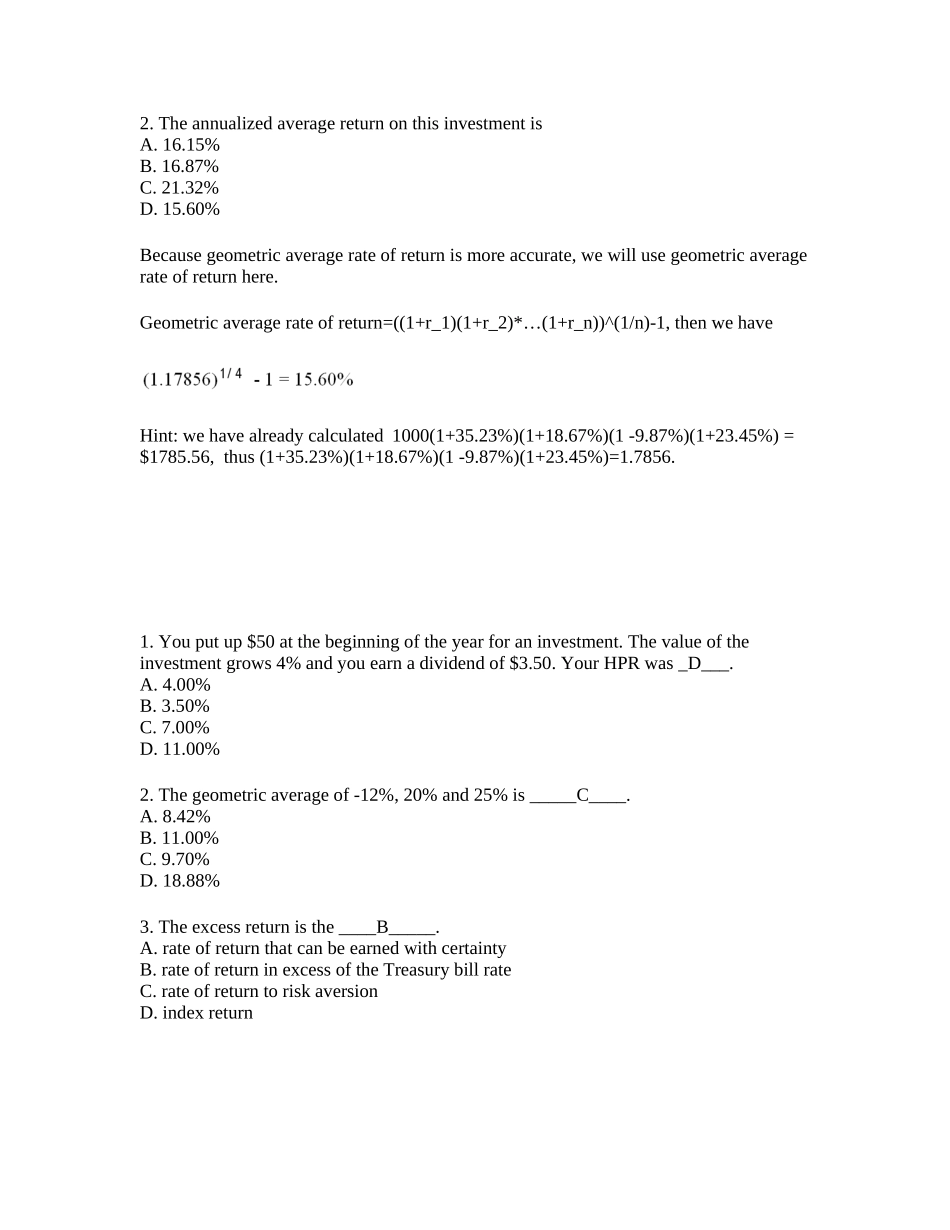

TheannualizedaveragereturnonthisinvestmentisA

60%Becausegeometricaveragerateofreturnismoreaccurate,wewillusegeometricaveragerateofreturnhere

Geometricaveragerateofreturn=((1+r_1)(1+r_2)*…(1+r_n))^(1/n)-1,thenwehaveHint:wehavealreadycalculated1000(1+35

23%)(1+18

67%)(1-9

87%)(1+23

45%)=$1785

56,thus(1+35

23%)(1+18

67%)(1-9

87%)(1+23

45%)=1