6-1 Chapter 6 Audit Responsibilities and Objectives Review Questions 6-1 The objective of the audit of financial statements by the independent auditor is the expression of an opinion on the fairness with which the financial statements present financial position, results of operations, and cash flows in conformity with generally accepted accounting principles

The auditor meets that objective by accumulating sufficient appropriate evidence to determine whether the financial statements are fairly stated

6-2 It is management's responsibility to adopt sound accounting policies, maintain adequate internal control and make fair representations in the financial statements

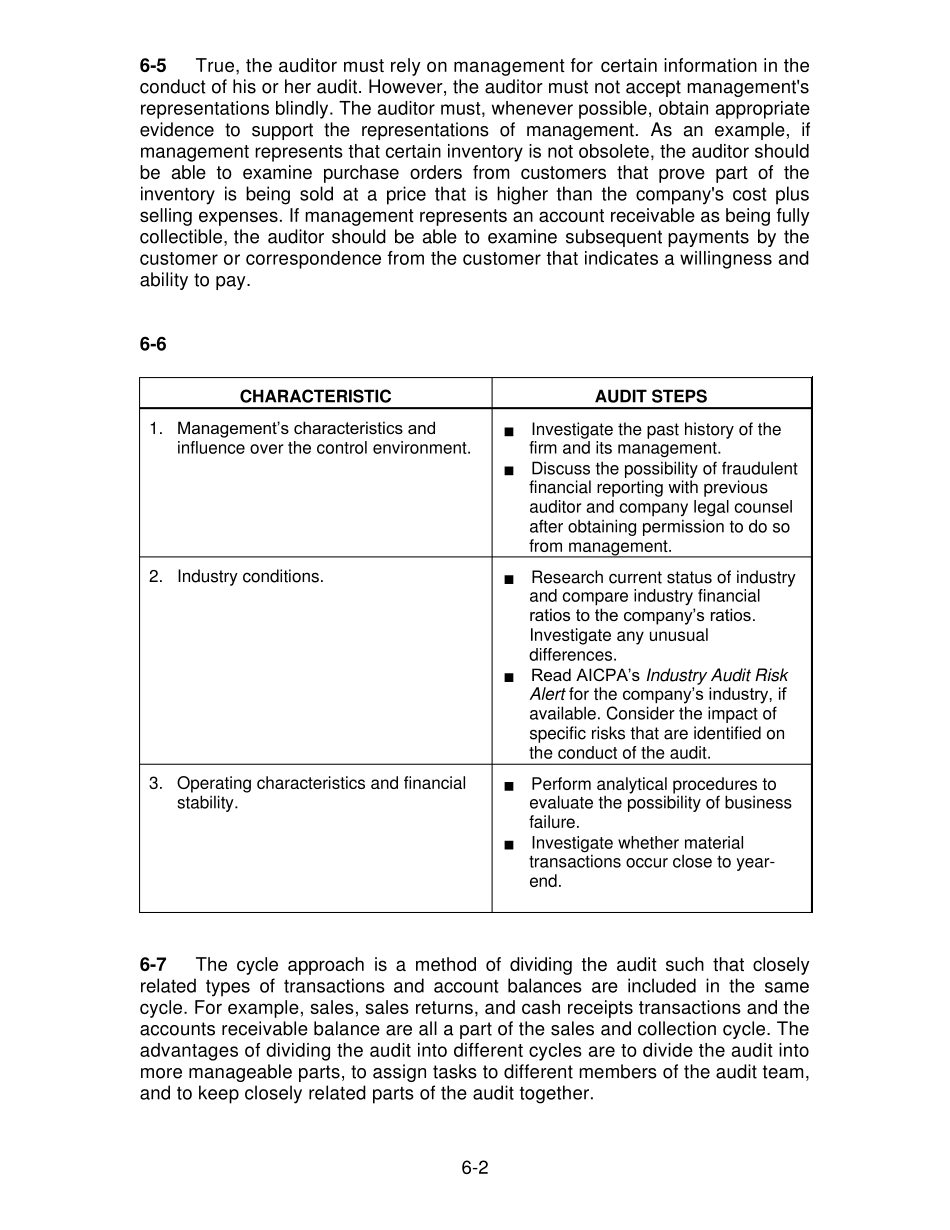

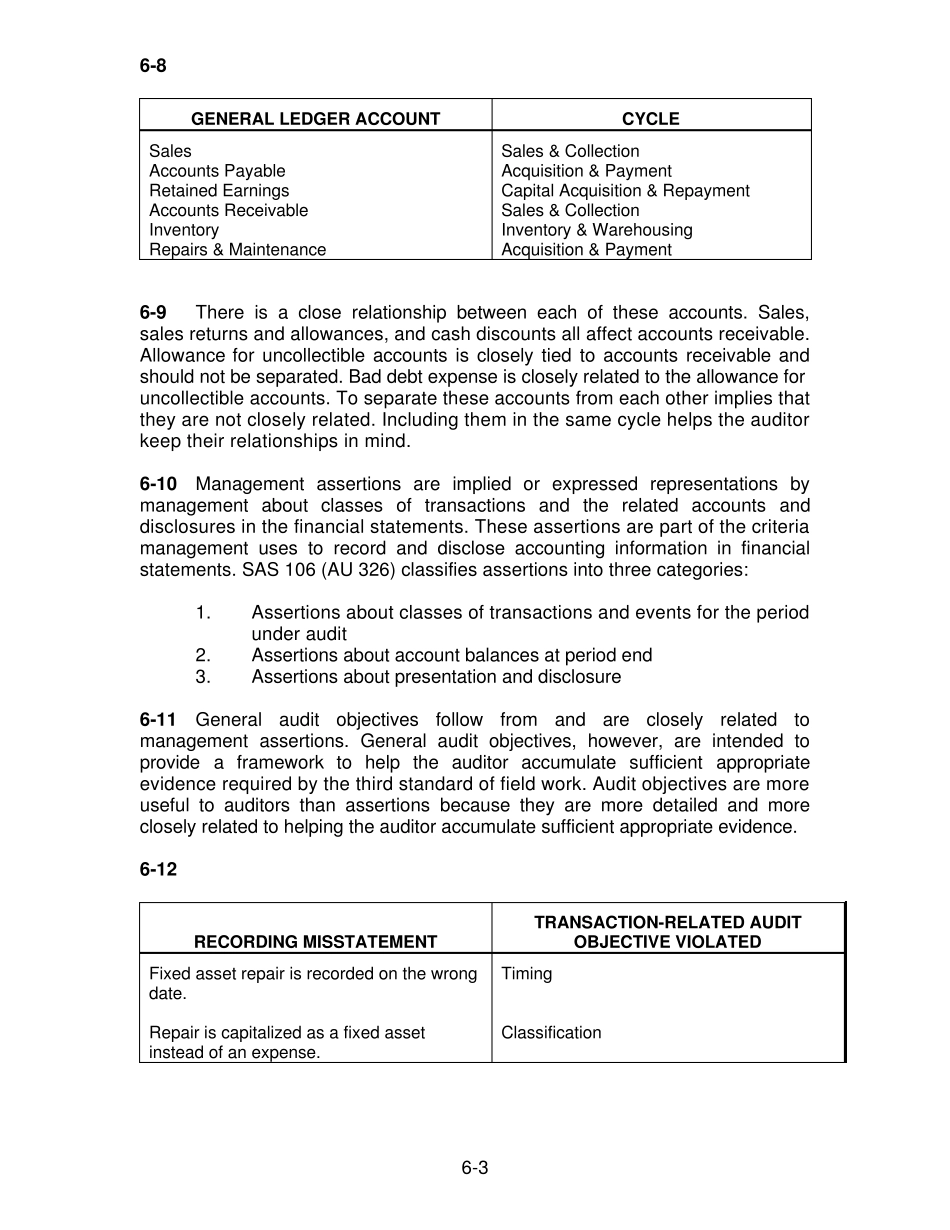

The auditor's responsibility is to conduct an audit of the financial statements in accordance with auditing stan