Determining HowCosts Behave如何決定成本習性Chapter 10Learning Objective 1Explain the two assumptionsfrequently used incost-behavior estimation

解釋經常運用在估計成本習性之兩種假設成本習性 成本習性:成本習性係指成本隨著作業量變動 而變動的方式

成本習性分析的目的 : 1

成本之計算 2

成本之控制 3

成本之規劃 4

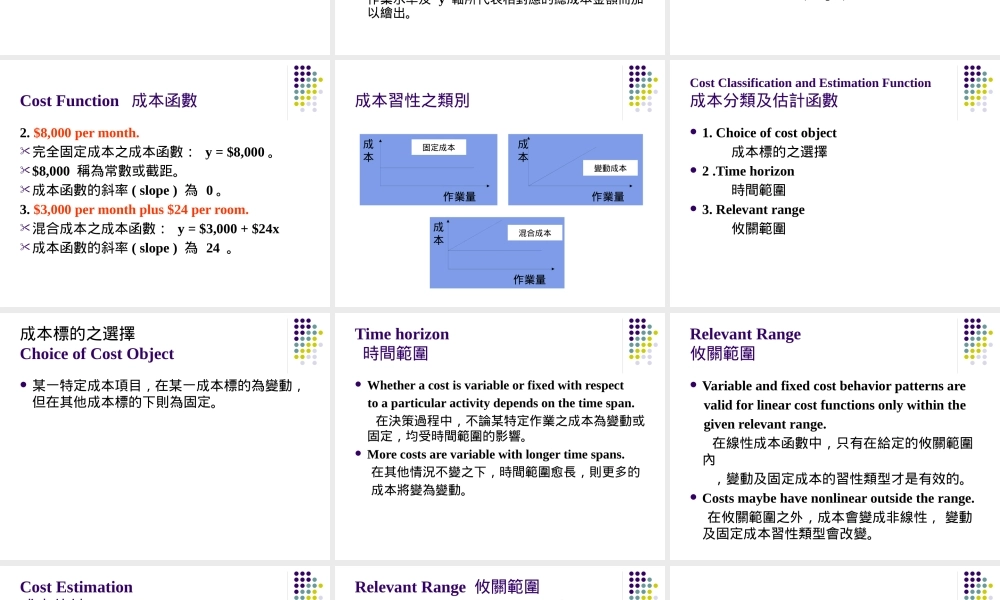

成本之分析 成本習性之類別: 1

固定成本 2

變動成本 3

混合成本Assumptions in Cost-Behavior Estimation成本行為估計之假設 1

Changes in total costs can be explained by changes in the level of a single activity

藉由單一作業水準之變動來解釋總成本的變 動

Cost behavior can adequately be approximated by a linear function of the activity level within the relevant range

在攸關範圍內,成本習性近似線性函數

Learning Objective 2Describe linear cost functions and three common ways in which they behave描述線性成本函數及三種常用之函數Cost Function 成本函數 What is a cost function

何謂成本函數

It is a mathematical expression describing how costs change with chan