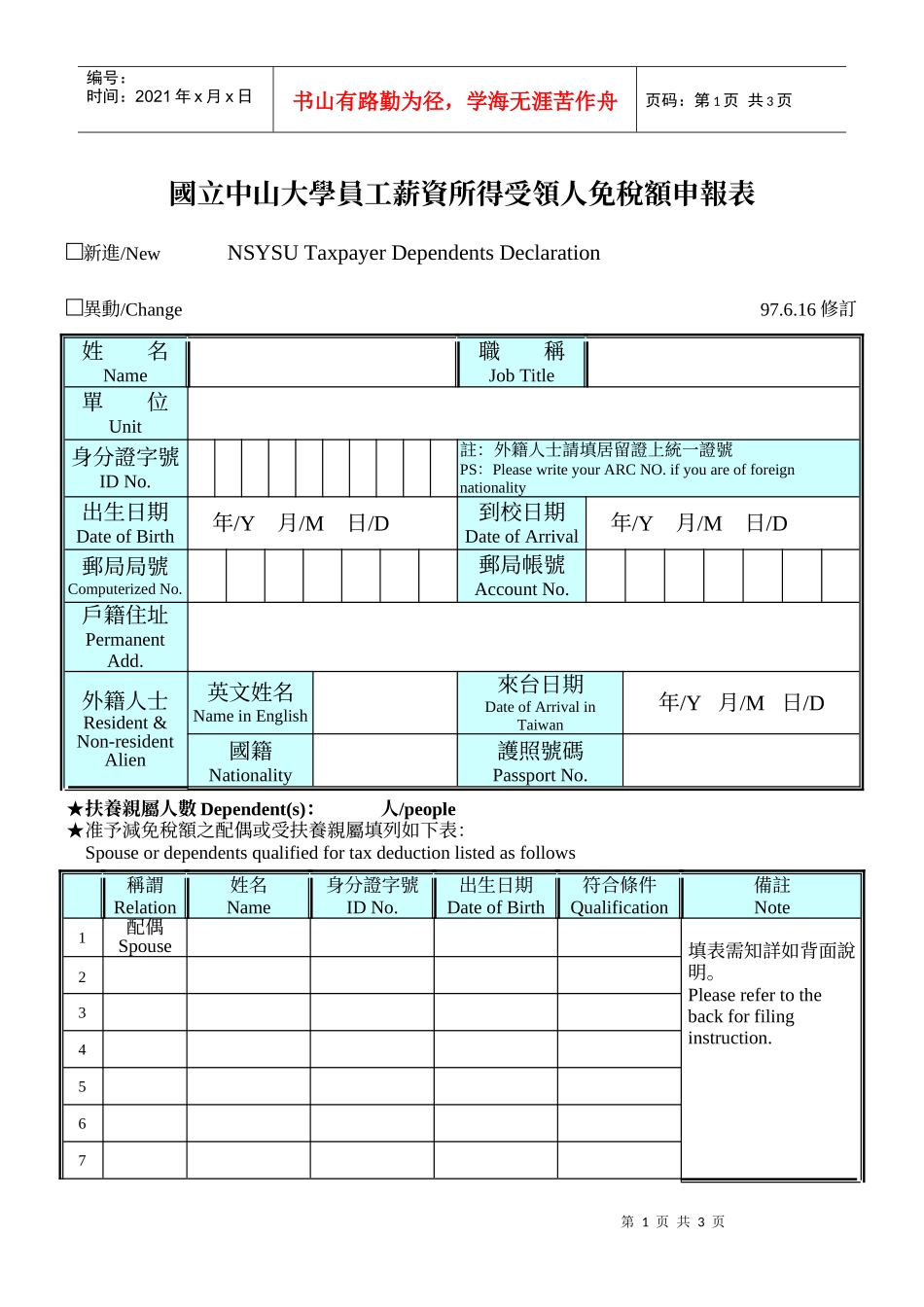

第1页共3页编号:时间:2021年x月x日书山有路勤为径,学海无涯苦作舟页码:第1页共3页國立中山大學員工薪資所得受領人免稅額申報表□新進/NewNSYSUTaxpayerDependentsDeclaration□異動/Change97

16修訂姓名Name職稱JobTitle單位Unit身分證字號IDNo

註:外籍人士請填居留證上統一證號PS:PleasewriteyourARCNO

ifyouareofforeignnationality出生日期DateofBirth年/Y月/M日/D到校日期DateofArrival年/Y月/M日/D郵局局號ComputerizedNo

郵局帳號AccountNo

戶籍住址PermanentAdd

外籍人士Resident&Non-residentAlien英文姓名NameinEnglish來台日期DateofArrivalinTaiwan年/Y月/M日/D國籍Nationality護照號碼PassportNo

★扶養親屬人數Dependent(s):人/people★准予減免稅額之配偶或受扶養親屬填列如下表:Spouseordependentsqualifiedfortaxdeductionlistedasfollows稱謂Relation姓名Name身分證字號IDNo

出生日期DateofBirth符合條件Qualification備註Note1配偶Spouse填表需知詳如背面說明

Pleaserefertothebackforfilinginstruction

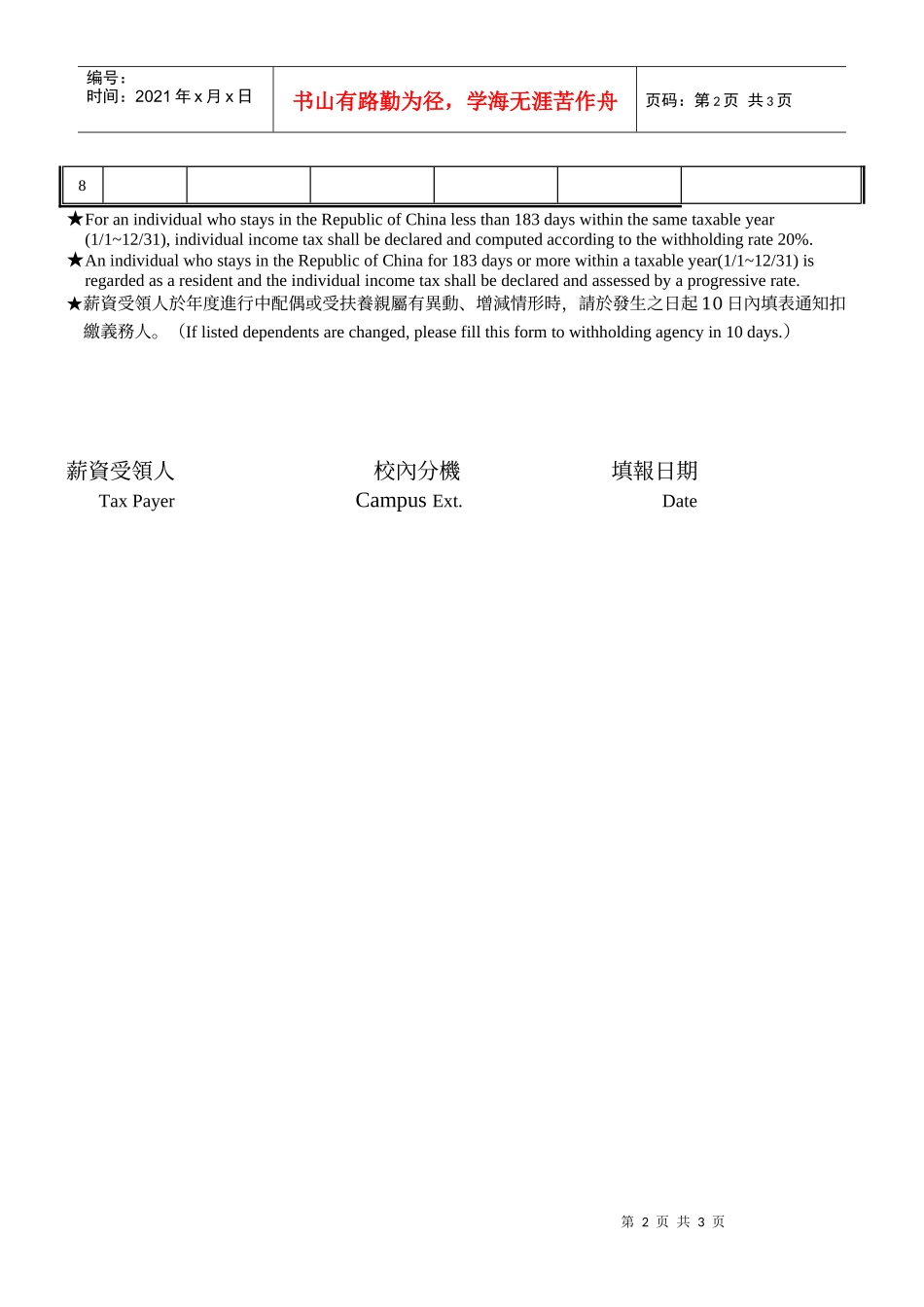

234567第2页共3页第1页共3页编号:时间:2021年x月x日书山有路勤为径,学海无涯苦作舟页码:第2页共3页8★ForanindividualwhostaysintheRepublicofChinalessthan183dayswithinthesametax