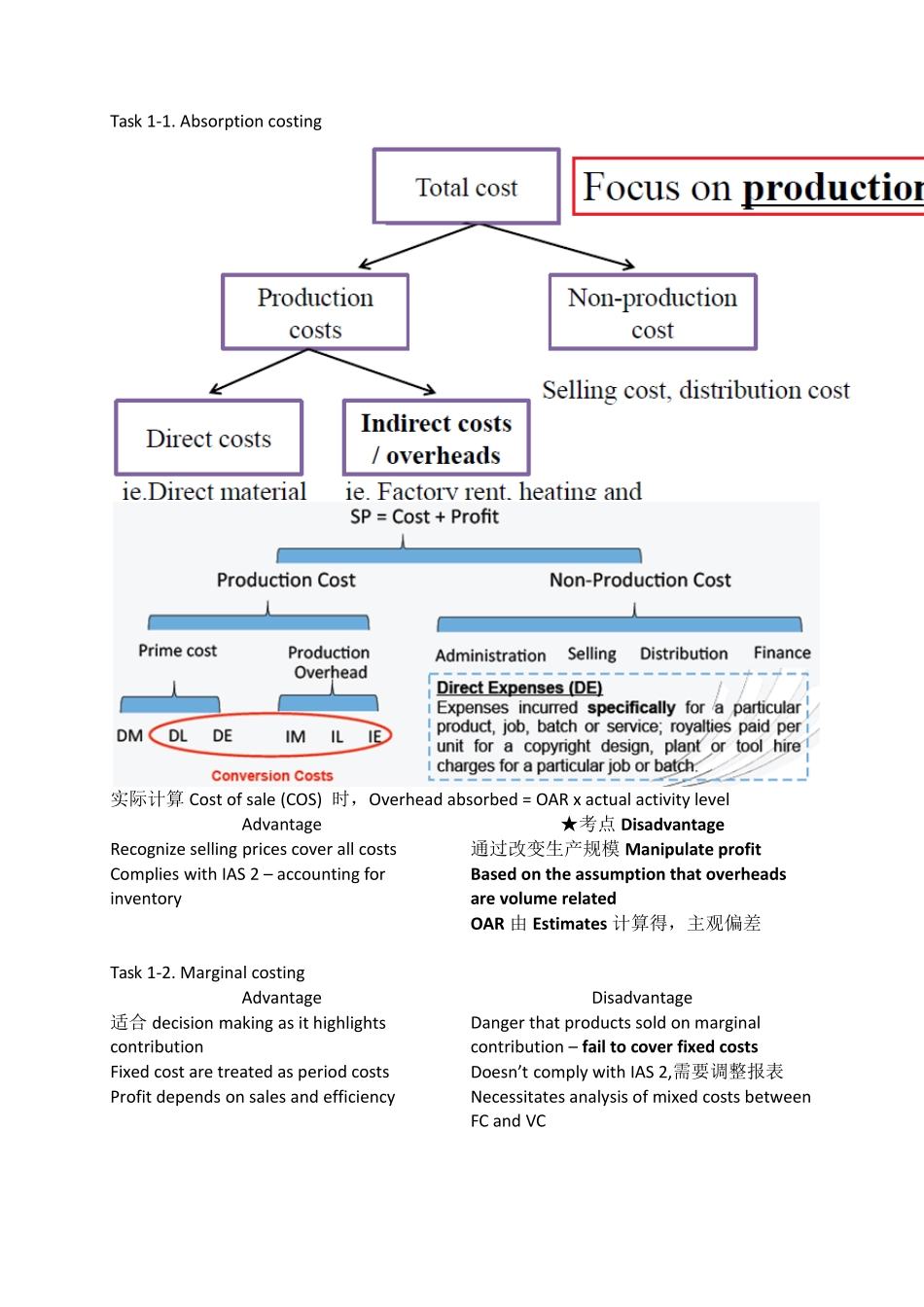

Task 1‐1

Absorption costing OAR= Estimated Production Overhead / Estimated Activity Level,都是budget 值 *Activity level 可以是production units,可以是labor hours,也可是machine hours 取决于劳动密集,还是机械生产密集intensive

实际计算Cost of sale (COS) 时,Overhead absorbed = OAR x actual activity level Advantage ★考点 Disadvantage Recognize selling prices cover all costs 通过改变生产规模 Manipulate profit Complies with IAS 2 – accounting for inventory Based on the assumption that overheads are volume related OAR 由 Estimates 计算得,主观偏差 Task 1‐2

Marginal costing Advantage Disadvantage 适合 decision making as it highlights contribution Danger that products sold on marginal contribution – fail to cover fixed costs Fixed cost are treated as period costs Doesn’t comply with IAS 2,需要调整报表 Profit depends on sales and efficiency Necessitates ana