Chapter10Derivatives:RiskManagementwithSpeculation,Hedging,andRiskTransfer1

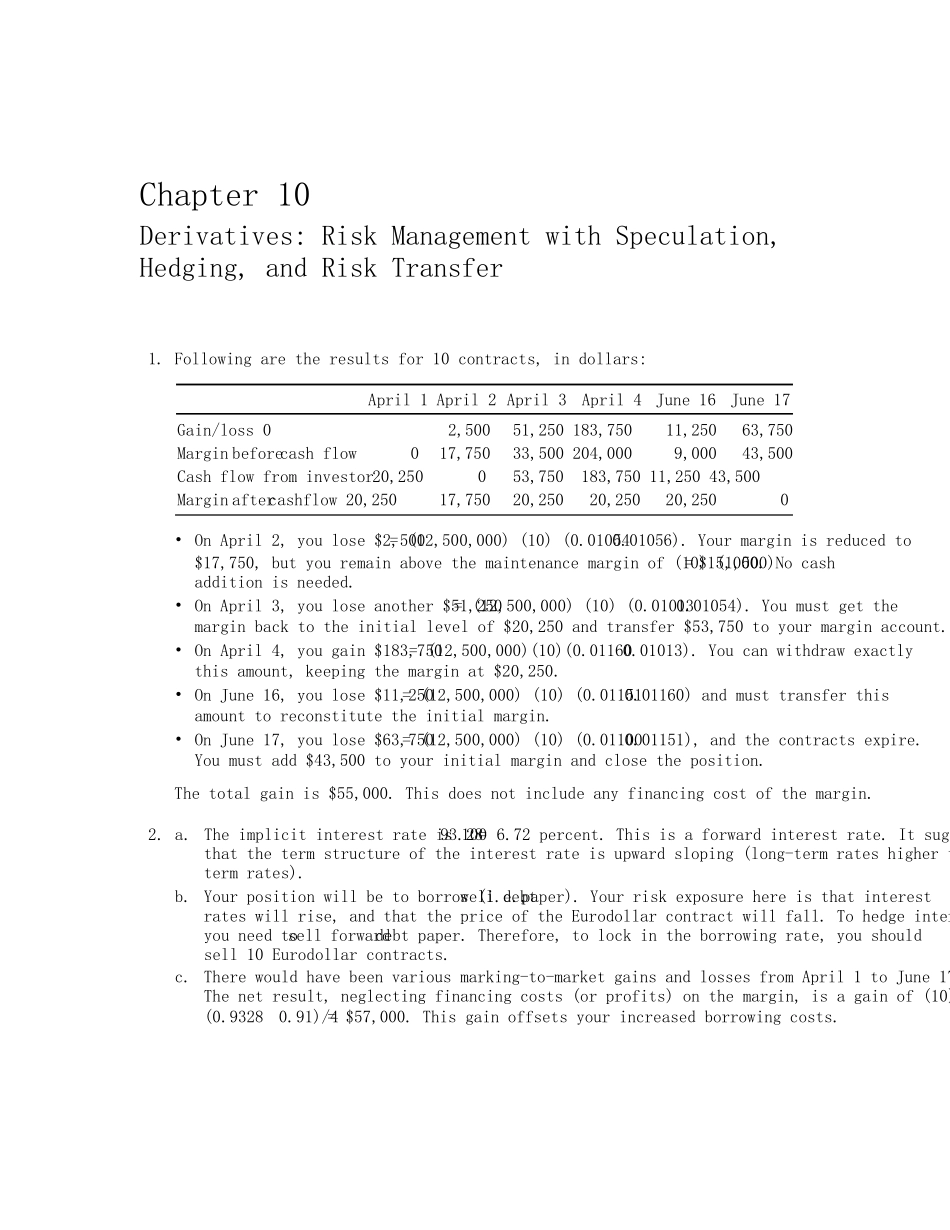

Followingaretheresultsfor10contracts,indollars:April1April2April3April4June16June17Gain/loss0−2,500−51,250183,750−11,250−63,750Marginbeforecashflow017,750−33,500204,0009,000−43,500Cashflowfrominvestor20,250053,750−183,75011,25043,500Marginaftercashflow20,25017,75020,25020,25020,2500•OnApril2,youlose$2,500=(12,500,000)(10)(0

01054−0

01056)

Yourmarginisreducedto$17,750,butyouremainabovethemaintenancemarginof(10)(1,500)=$15,000

Nocashadditionisneeded

•OnApril3,youloseanother$51,250=(12,500,000)(10)(0

01013−0

01054)

Youmustgetthemarginbacktotheinitiallevelof$20,250andtransfer$53,750toyourmarginaccount

•OnApril4,yougain$183,750=(12,500,000)(10)(0

01160−0

01013)

Youcanwithdrawexactlythisamount,keepingthemarginat$20,250