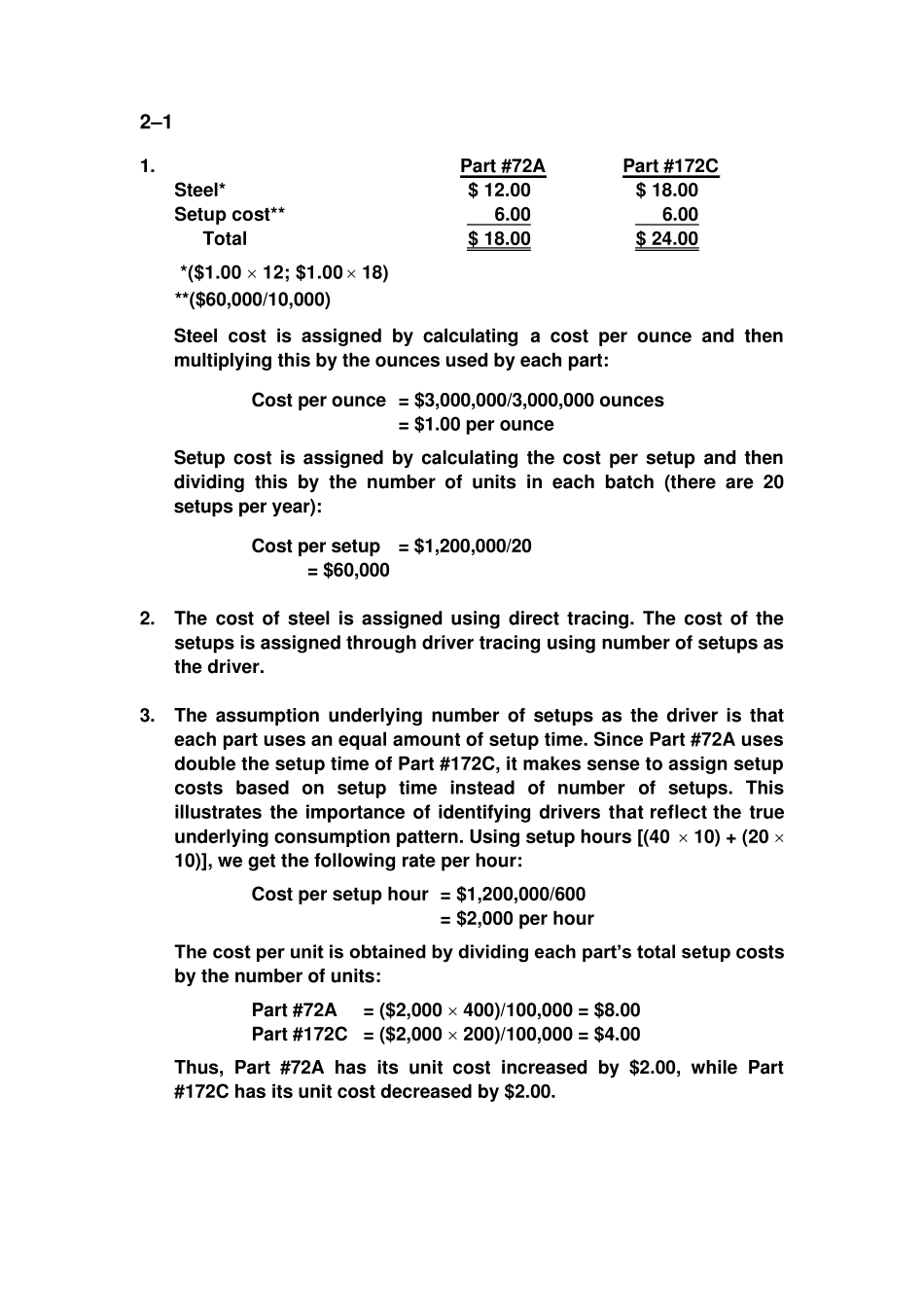

Part #72A Part #172C Steel* $ 12

00 $ 18

00 Setup cost** 6

00 Total $ 18

00 $ 24

00 *($1

00 12; $1

00 18) **($60,000/10,000) Steel cost is assigned by calculating a cost per ounce and then multiplying this by the ounces used by each part: Cost per ounce = $3,000,000/3,000,000 ounces = $1

00 per ounce Setup cost is assigned by calculating the cost per setup and then dividing this by the number of units in each batch (there are 20 setups per year): Cost per setup = $1,200,000/20 = $60,000 2

The cost of steel is assigned using direct tracing

The cost of the setups is assigned through driver tracing using number of setups as the driver

The assumption underlying number of setups as the driver is that each part uses an equal amount of setup time

Since Part #72A uses double