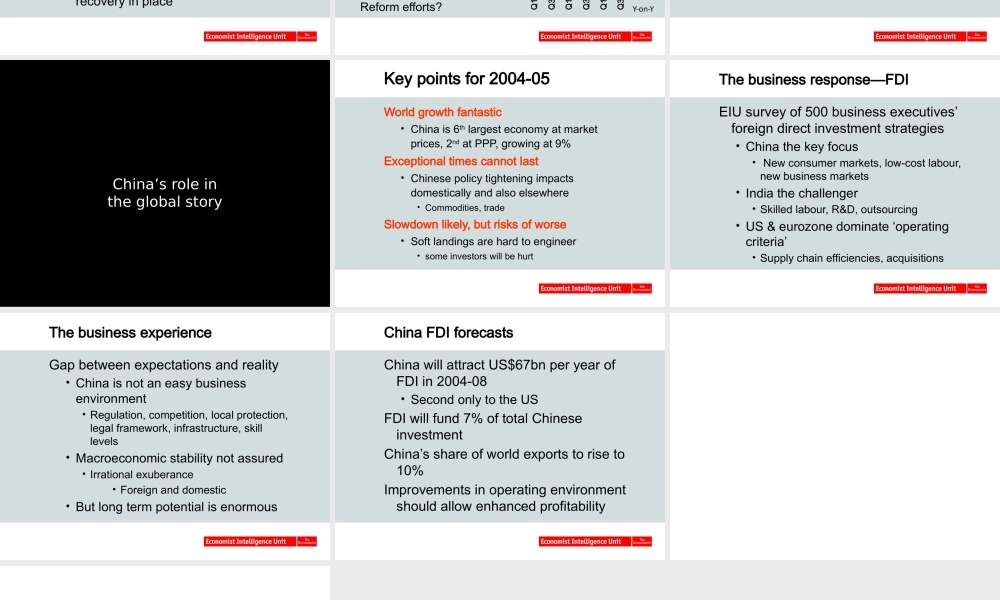

China and the global economyWhy ignoring China is no longer an option

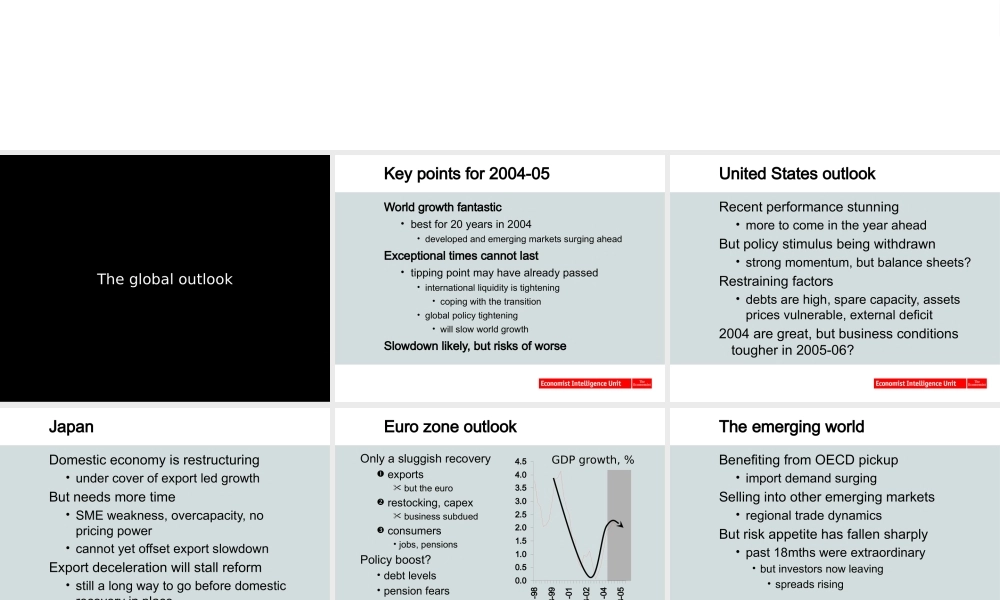

Robin Bew, Chief EconomistJune 2004The global outlookKey points for 2004-05World growth fantastic best for 20 years in 2004 developed and emerging markets surging aheadExceptional times cannot last tipping point may have already passed international liquidity is tightening coping with the transition global policy tightening will slow world growthSlowdown likely, but risks of worseUnited States outlookRecent performance stunning more to come in the year aheadBut policy stimulus being withdrawn strong momentum, but balance sheets

Restraining factors debts are high, spare capacity, assets prices vulnerable, external deficit2004 are great, but business conditions tougher in 2005-06

JapanDomestic economy is res