Straight-line depreciation 1

what is the straight-line depreciation

Straight-line depreciation is the simplest and most often used method

In this method, the company estimates the salvage value of the asset at the end of the period during which it will be used to generate revenues (useful life)

(what is the salvage value: The salvage value is an estimate of the value of the asset at the time it will be sold or disposed of; it may be zero or even negative

Salvage value is also known as scrap value or residual value

) The company will then charge the same amount to depreciation each year over that period, until the value shown for the asset has reduced from the original cost to the salvage value

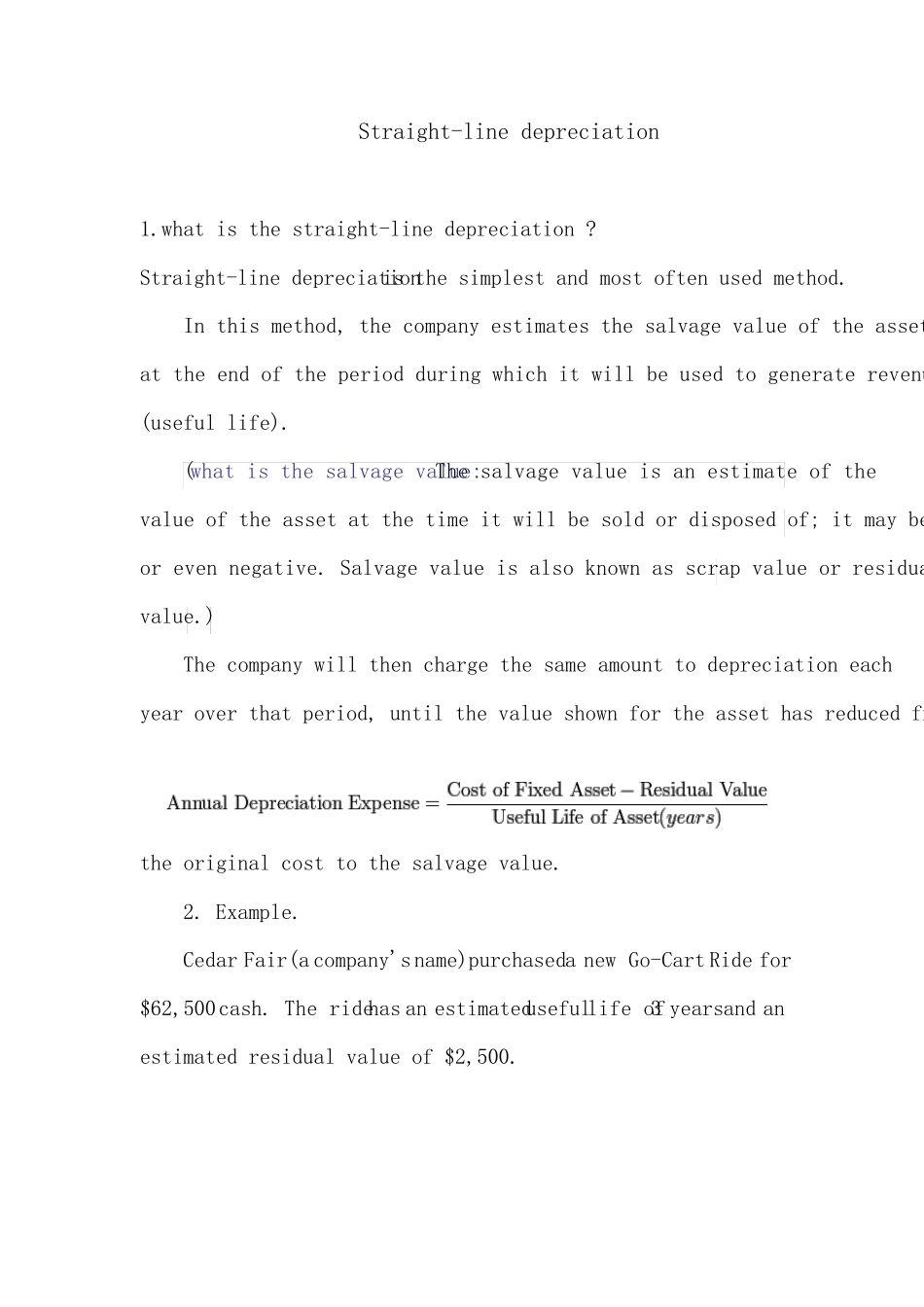

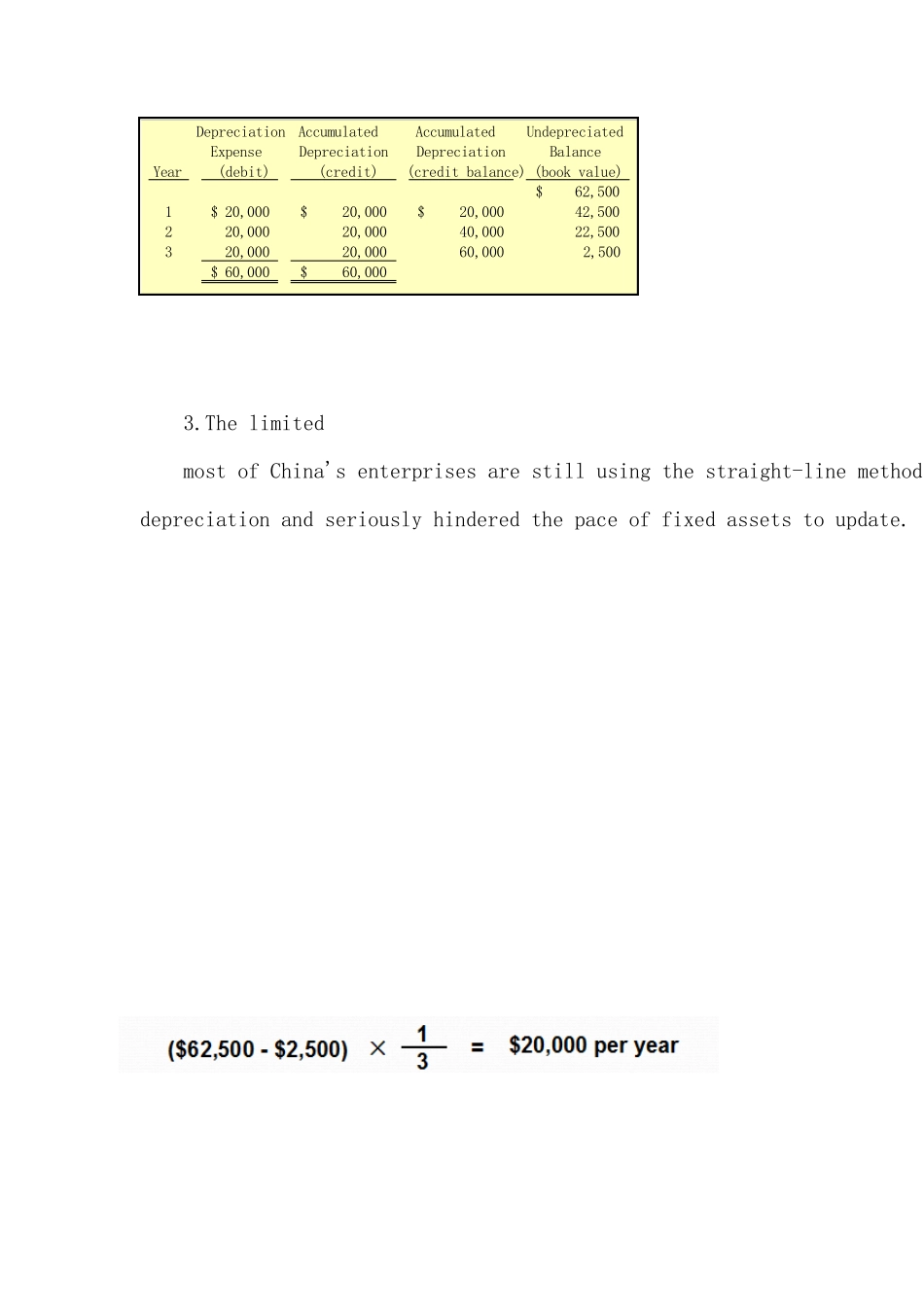

Example

Cedar Fair (a company's name)purchased a new Go-Cart Ride for $62,500 cash