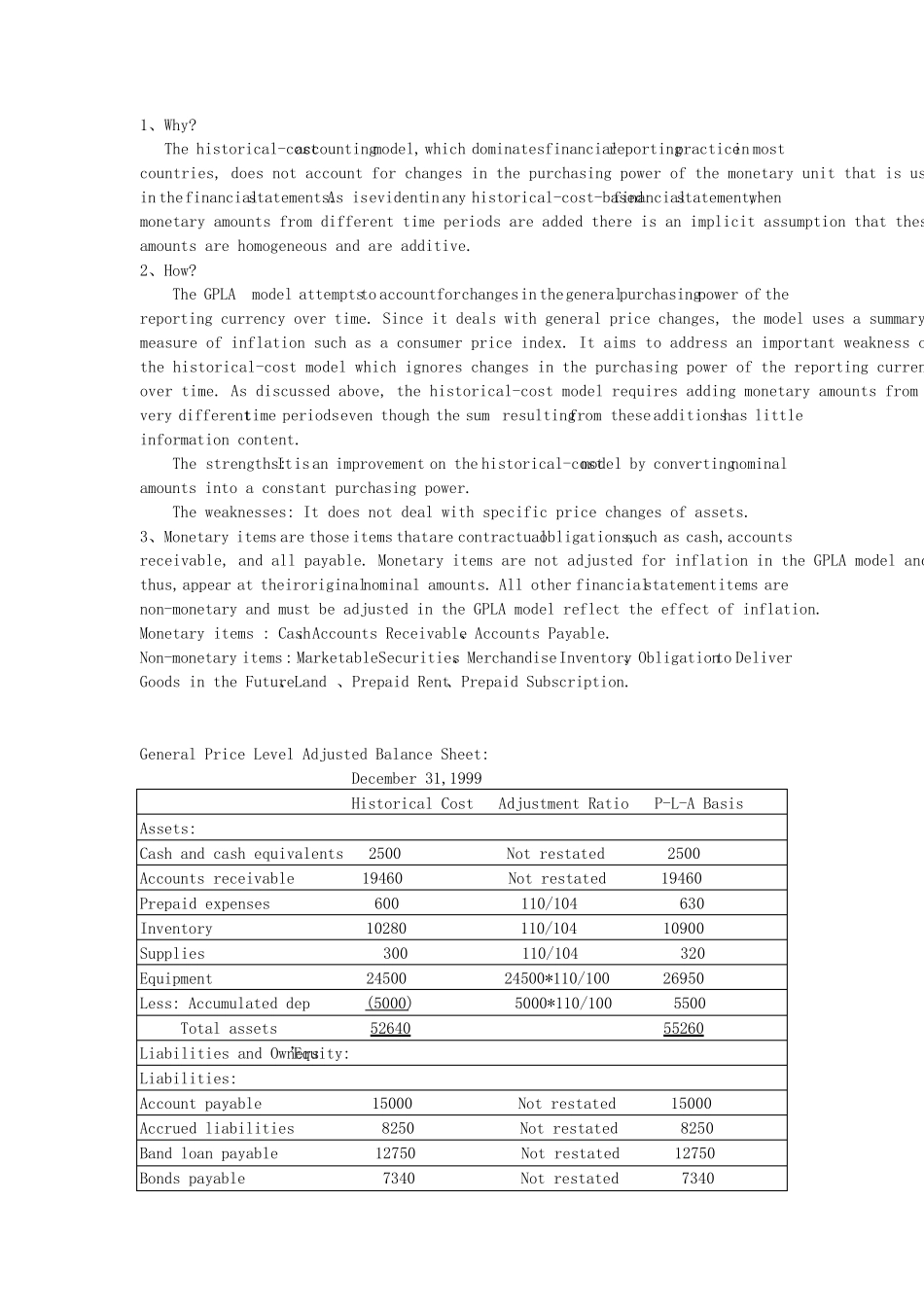

1、 Why

The historical-cost accounting model, which dominates financial reporting practice in most countries, does not account for changes in the purchasing power of the monetary unit that is used in the financial statements

As is evident in any historical-cost-based financial statement, when monetary amounts from different time periods are added there is an implicit assumption that these amounts are homogeneous and are additive

2、 How

The GPLA model attempts to account for changes in the general purchasing power of the reporting currency over time

Since it deals with general price changes, the model uses a summary measure of inflation such as a consumer price index

It aims to address an important weakness of the historical-cost model which ignores changes in the purchasing power of t